United Kingdom equities

Gauging how the UK could perform relative to other markets requires understanding of its unique sector composition rather than just assessing the specifics of its macro environment.

The UK is facing some specific headwinds such as the broadly held perception that there will be a change in prime minister. We think the most likely replacement is Andy Burnham who has served as the mayor of Manchester. Burnham is perceived as being a less market-friendly candidate as he has expressed support for nationalising utilities and introducing asset-based taxes. His policies seem likely to result in more government borrowing, in our opinion, the case for which needs to be compelling given an already-high debt-to-GDP ratio and rising interest expense.

The debate over who will be the next prime minister chosen from the ruling Labour Party masks even greater uncertainty over who will win the next election (not due until 2029) as the two traditional Labour and Conservative parties which split 57% of the vote in 2024, only amass 37% in total in recent polls.

Despite the international nature of the UK equity market, fund flows into the asset class tend to be correlated to the domestic economy, using the UK composite Purchasing Managers’ Index as a proxy. Accordingly, the political overhang and weak domestic growth picture, are likely to hold back flows into UK equities near term, in our view.

Also, for many years, UK investors have been gradually unwinding their home bias (preferring stocks based in one’s own country versus those domiciled in other countries), leading to persistent selling pressure in the UK market. This partly reflects the distinctive sector composition of the UK equity market. Relative to the global market, it has virtually no Information Technology exposure. Because of this, it has suffered very little from the slide in software stocks but benefitted even less from the rise in hardware and AI stocks. It does, however, have meaningful exposure to important sectors and industries such as Energy, Health Care (pharmaceuticals), and Consumer Staples. These UK sectors have performed very similarly to global peers.

We think the most obvious industry that closely reflects the UK economy is banks, which makes up about 16% of the equity market. UK banks are distinct from peers in other markets because their valuations look significantly cheaper and yet they achieve similar profitability.

It’s difficult to see the UK fully emerging from the gloom of political uncertainty over the coming months. However, when global equity market conditions seem stretched in the areas Britain is not exposed to such as Information Technology and AI stocks specifically, we believe there is potential for outperformance as has been the case during such periods in previous years.

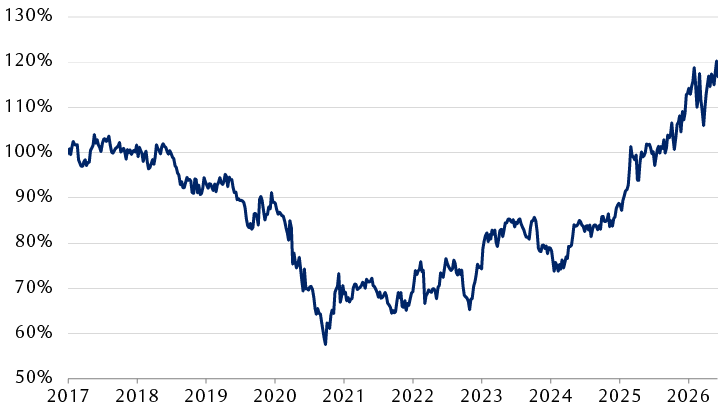

UK banks outperform despite the domestic gloom

Relative total return of LSEG’s UK-DS Banks vs. World DS-Banks

Source - RBC Wealth Management, LSEG; data through 6/5/26

The chart shows the performance of UK banks relative to global banks from 2017 through June 5, 2026. The relative performance of UK banks declined from 2018 through late 2020, then trended unevenly upward through 2024; the upward trend has been more stable through June 2026.

United Kingdom fixed income

The UK is facing an energy price shock when softer consumer demand and a less tight labour market, in our view, are reducing the risk of higher prices feeding through into broader wage pressures as was the concern three years ago. Indeed, the Bank of England’s (BoE) May Decision Maker Panel survey pointed to expectations of modestly lower inflation over the coming 12 months, but more importantly, the downward trend in employment and wage growth continues. With monetary policy already restrictive at 3.75%, the BoE has room, in our view, to tighten by less than the current cumulative 35 basis points (bps) priced in by markets by December 2026.

We see two possible scenarios for H2 2026. First, inflation returns to the BoE’s 2% target over a two-year horizon, accompanied by modest second-round wage pressures and weak growth. This is our base case, and we expect one rate hike from the BoE this year. Second, the most severe scenario, in our opinion, would be a prolonged conflict with a resolution in limbo, sustained elevated energy prices, surging inflation, and contracting economic growth. This would prompt additional tightening amid heightened second-round wage pressures. We note that longer-dated market inflation expectations currently remain well anchored, with markets treating the energy shock as largely transitory, limiting the risk of persistent second-round effects.

April’s public finances figures showed a worsening fiscal outlook as borrowing overshot forecasts. We project further fiscal pressure due to higher bond yields (now trading between 55–80 bps higher across the yield curve since Feb. 27), targeted energy support measures, and a weakening economy. Though we have likely seen peak Gilt issuance, with supply skewed away from longer-dated bonds, we maintain an Underweight in longer-dated bonds. For long-term investors, opportunities exist to lock in attractive yields when bond yields appear elevated beyond what fundamentals justify.

While bond supply is less of a headwind in the UK compared to the U.S. and Europe, high issuance in the Technology sector has limited credit spread tightening, compared to other sectors which are trading at much tighter levels. We believe credit spreads could widen from here due to energy cost pass-through uncertainty, weaker growth, and political risks. We prefer an Underweight position in corporate bonds, favouring exposure in defensive sectors over cyclicals.