After many months of tariff angst in 2025, we’re right back near the level that then-presidential candidate Donald Trump originally campaigned on in 2024.

The U.S. average effective tariff rate on other countries hovers around 9.9 to 10.5 percent, according to estimates by the Tax Foundation and Penn Wharton Budget Model, which consider actual tariffs paid to U.S. customs and consumers’ changes in purchasing patterns when confronted with higher-priced goods.

This range is well below the 20-plus percent estimates that were penciled in by many economists following the sky-high “reciprocal” tariff levels announced in April 2025, the peak period of market angst. Since then, the rate has dropped following U.S. trade deals with key partners such as the EU, Japan, and South Korea, among others, and an important trade truce with China.

Although the roughly 10 percent level is lower than feared, it represents a sea change compared to the declining and low tariff rates during much of the post-World War II era. Currently, it is the loftiest level since 1946 and well above 2.4 percent in 2024, before President Trump’s second term began.

It would be in keeping with the administration’s character to issue additional tariff threats periodically this year, including ahead of the United States-Mexico-Canada Agreement (USMCA) mandatory review in July.

But we doubt the average U.S. effective tariff rate will rise much—if at all—ahead of the November midterm elections given the political sensitivities associated with the affordability issue and the desire to pull down inflation further.

Who is actually paying the tariffs?

RBC Global Asset Management economists assess that foreign and domestic companies have been sharing the tariff burden by a roughly 50/50 percent split.

Within that balance, about one-third of tariff costs have been passed on to American consumers via higher goods prices, based on an analysis of data through September 2025.

RBC economists anticipate tariff pass-through will continue this year, which should keep the Consumer Price Index (CPI) and other consumer inflation measures somewhat elevated above the Federal Reserve’s preferred level.

“On the whole, however, the impact of tariffs on growth and CPI looks like it will ultimately be less than models originally suggested,” according to RBC Global Asset Management Inc. Senior Economist Josh Nye.

What does this mean for Americans’ wallets? Assessments vary.

The Tax Foundation estimates that tariffs represent an average tax increase of $1,000 in 2025 and $1,300 in 2026 per household, based on tariff rates through the latter part of January.

The Tax Policy Center, a joint effort by the Urban Institute and Brookings Institution, sees a greater hit in its recently updated forecast. It estimates the Trump 2.0 tariffs will represent an average $2,100 burden per household in 2026.

SCOTUS to weigh in soon

The U.S. Supreme Court is expected to rule on the administration’s use of the International Emergency Economic Powers Act (IEEPA), the instrument by which the bulk of the Trump 2.0 tariffs have been implemented.

Even if the Court were to rule against the administration’s IEEPA use, RBC Global Asset Management Inc. Chief Economist Eric Lascelles wrote, “…the reality is that the U.S. can virtually instantaneously introduce temporary 15% tariffs and then, after some obligatory research and hearings, impose just about whatever tariff rate it desires at a later date. Thus, the White House should be able to get where it wants to go even without the convenience of IEEPA tariffs.”

Lascelles believes the Court is “quite unlikely” to require tariff reimbursements as this would be “chaotic as most businesses have passed at least a portion of their tariff costs up and down the supply chain, with no clear way to properly compensate other parties.”

Are tariffs here to stay?

Polls show the Trump 2.0 tariffs lack popularity, with 60 percent of Americans disapproving of them, according to Pew Research.

Ahead of the midterm elections, Congress is pushing back. The House of Representatives recently voted by a very narrow margin to terminate the IEEPA tariffs on Canada. More tariff votes in the House and Senate seem in the offing this year; Trump holds the veto pen, however.

We think it will be tempting for the next president—regardless of party—to keep in place at least some or most of the Trump 2.0 tariffs, as they are now an important federal government revenue stream.

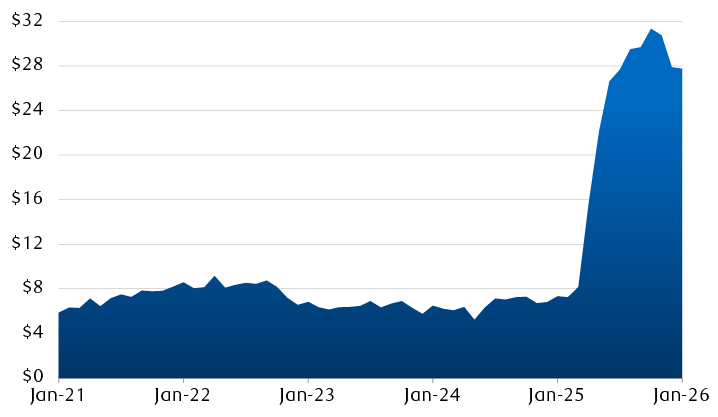

In January 2026, the $27.74 billion in tariff revenue was almost four times the average from 2021 to 2024, according to customs data compiled by the U.S. Department of the Treasury, calculated on a “conventional basis”—meaning the actual dollars coming into customs, without negative side effects being taken into consideration.

Tariff revenue has surged

Net customs receipts to U.S. government by month ($ billions)

Source - RBC Wealth Management, U.S. Department of the Treasury, Bloomberg; monthly data through 1/31/26

The chart shows monthly customs receipts from January 2021 through January 2026. In January 2021 receipts began at $5.87 billion. Collections crept somewhat higher through early 2022 and then started drifting a bit lower later that year and reached a low point of $5.23 billion in May 2024. From 2021 through 2024 receipts averaged $7.08 billion per month. In April 2025 tariff revenues began to spike, reaching a high of $31.35 billion in October 2025. By January 2026 they had pulled back to $27.74 billion.

The government collected $264 billion in net customs revenue in 2025, and the amount should be a lot higher in 2026, the first full year under the Trump 2.0 tariff framework.

If the current tariffs remain in place, the Tax Foundation forecasts they will raise over $2.1 trillion in federal revenue on a conventional basis from 2026 through 2035 (or $1.44 trillion on a “dynamic basis” when negative side effects are considered).

Some deficit relief but not a panacea

The tariff revenue surge helped decrease the U.S. fiscal deficit. It declined to 5.4 percent of GDP in 2025 from 6.9 percent in 2024, based on preliminary data.

But this is still a relatively big number—far from Treasury Secretary Scott Bessent’s goal of around three percent of GDP by 2028 and well above the two percent level we would consider palatable.

The Congressional Budget Office forecasts a 5.8 percent deficit-to-GDP ratio in 2026, an increase to 6.0 percent in 2028, and an even higher level in 10 years.

It would take a lot more than tariff revenue to right-size the deficit given spending is high and growing on Medicare, Medicaid, Social Security, and defense, among other programs. Also, net interest payments on the federal debt remain sizeable, at 13.9 percent of expenditures so far in fiscal year 2026.

The country hasn’t seen spending discipline since a brief period in the 1990s, and unfortunately, we don’t think this will change anytime soon, regardless of which party is in power—unless the Treasury market forces Washington’s hand.

Our fixed income team anticipates that institutional investors around the world will keep a closer eye on the U.S. federal deficit and debt levels than they did in previous years and that sizeable deficits will keep long-term Treasury yields, particularly the 30-year maturity, higher than they would be otherwise.