United States

Alan Robinson – Seattle

U.S. stock indexes started the week on a positive footing as investors assumed the long-awaited announcement on new tariffs would be more bark than bite. But the eventual release of the new proposed schedule on Wednesday, April 2 after the market close was much worse than expected and took a significant chunk out of the stock market.

Participants had expected a roughly 10 percent tariff across most trading partners, with higher rates for China, for a weighted effective tariff rate of 17 percent. The final announcement delivered sweeping increases across 60 countries with many facing rates above 30 percent. Asian exporters were particularly hard hit. Wall Street economists calculated the weighted average tariff levied by the U.S. would increase tenfold to 24 percent to 26 percent compared to the 2.5 percent rate levied in 2024.

Asia hit hardest by new U.S. tariffs

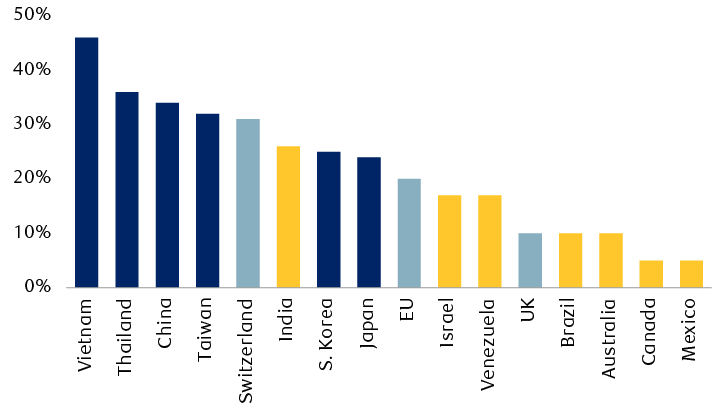

Newly announced U.S. tariffs on selected countries

This bar cart displays the new U.S. tariffs announced April 2, 2025 on 16 selected countries. The tariffs range from 46% levied on imports from Vietnam to 5% on Canada and Mexico.

Source - RBC Wealth Management, White House

RBC Capital Markets, LLC Head of U.S. Equity Strategy Lori Calvasina weighed the impact of the announcement in terms of headwinds to the equity market, and offered some thoughts as to why equity investors might find partial relief in some of the details of the tariff proposals.

The clear negatives include the blanket nature of the tariffs and the lack of carveouts for certain industry segments. This is likely compounded by the lack of clarity for analysts as to what the ultimate tariff levels will be. She suggests this may have knock-on effects as consumers and businesses hold off on spending and investment plans until a sustainable tariff regime is settled. Other issues include the potential for retaliatory tariffs from trading partners, particularly if these measures are designed as a starting point for negotiations. It’s unlikely other countries would want to initiate negotiations from a position of weakness, and retaliatory tariffs might level the playing field. In combination, we think these elements suggest rough sailing in the near term for the economy and markets, a point underscored by the administration in emphasizing the need to tolerate short-term pain to achieve its longer-term goals.

There were some potential brights spots in the announcement. The implementation date for the 10 percent baseline tariffs is April 5, and April 9 for the other, higher tariffs. This means a window for negotiation remains in place. There were also no higher tariffs announced for Canada and Mexico, with only imports outside of the USMCA agreement subject to tariffs, equivalent to a five percent effective rate for both countries. And finally, the tariff schedule does at least give corporate America something tangible to work with. This should allow management teams to communicate the likely impact on their businesses and provide guidance and visibility to stock investors, albeit at a more subdued level than the pre-tariff outlook.

The impact on financial markets was significant, with the S&P 500 Index down nearly five percent on Thursday. Technology stocks were hit harder due to their exposure to Asian supply chains, with the Nasdaq Index down nearly six percent. Traditionally defensive sectors such as Consumer Staples, Health Care, and Utilities outperformed the broad market, while cyclical sectors including Consumer Discretionary (particularly apparel), Industrials, and Financials underperformed. Bonds rallied, with interest rates on the benchmark 10-year U.S. government bond falling 18 basis points to 4.00 percent at one point.

Oil and other commodities opened lower on global growth concerns, and the U.S. dollar weakened further. This currency weakness confounded traders as the conventional wisdom expected the dollar to rally on higher tariffs based on less demand for foreign currencies that would be needed to fund imports. But the somewhat capricious nature of this trade pivot appears to have triggered a flight of currency investors out of the U.S. leading to a weaker dollar. This move was seemingly condoned by the administration in comments stating a weaker dollar would make U.S. exports more competitive.

However, if these tariffs trigger higher U.S. inflation, we think the Federal Reserve may err on the side of caution with respect to interest rate policy, and hesitate to cut short-term rates further. This may support the dollar against a backdrop of falling interest rates elsewhere.

Where from here? Economists and traders are still calculating the likely impact of the new tariffs. Initial estimates from our research correspondents suggest they will reduce U.S. economic growth by between 1.5 percent and 2.0 percent over a two-year period, and push inflation toward 5.0 percent from the current range of 2.5 percent to 3.0 percent, although much will depend on the longevity of the tariffs. The tariffs themselves may raise $700 billion to $800 billion annually if they do not cause trade volumes to slow, or approximately two percent of GDP. If these fees are reinvested into tax cuts or infrastructure, they could offset the negative hit to the economy; but if they are used to reduce the budget deficit, they would represent a significant fiscal tightening and lead to slower growth, in our view.

Calvasina warns that the break of the S&P 500 below the March 13, 2025 low near 5,500 opens the door to a more significant 14 percent to 20 percent “growth scare”-type drawdown from the Feb. 19, 2025 high near 6,150. If that were to occur, her year-end target of 6,200 might no longer be appropriate, with a year-end target a little above current levels perhaps more likely. In this environment we would continue to favor the more defensive areas of the equity market, including defensive stocks, value stocks, and dividend growers. Ultimately, this may be seen as an opportunity to invest in quality stocks for the long term, and we note that periods of extreme volatility are often among the best, if most uncomfortable, times to invest in stocks.

Canada

Nguyen Dang, CFA & Lindsay Puls – Toronto

The U.S. announced it had exempted Canada and Mexico from reciprocal tariffs through CUSMA/USMCA-compliant trade, though there are no guarantees this exemption will stay in place.

The U.S.’s existing 25 percent tariffs on steel and aluminum and USMCA-noncompliant goods, as well as a reduced 10 percent duty on USMCA-noncompliant energy and potash, remains in place.

Additionally, 25 percent auto tariffs on global imports have taken effect, pushing the average U.S. tariff rate on imports from Canada to about 3.5 percent from 2.5 percent, according to RBC Economics estimates.

The tariffs imposed on Canada came in lower than Street expectations, though further tariffs targeting semiconductors, pharmaceuticals, and critical minerals could be unveiled at a later date, according to White House officials.

According to RBC Economics, total tariffs imposed by the U.S. could lead to global disruptions, which could spill over to Canada and weaken production and price growth. Ongoing trade uncertainty is likely to weigh on Canadian corporate earnings and continue to cause short-term equity market volatility, in our view.

There are also uncertainties for the Canadian economy. Canadian GDP grew by 0.4 percent m/m in January, slightly ahead of Bloomberg consensus expectations and faster than the upwardly revised rate of 0.3 percent m/m from December. On a year-over-year basis, Canada’s economy grew at a 2.2 percent pace in each of the past two months, indicating to us that seven rounds of interest rate cuts over the past 10 months have helped boost consumer spending and investment. Both goods- and services-producing industries were up, with 13 of 20 sectors rising in January, according to Statistics Canada.

While Statistics Canada’s GDP report continued a series of encouraging economic results for Canada, January’s data reflects a pre-tariff environment, and soft survey data—such as the Conference Board’s Consumer Confidence Index—continues to indicate a likelihood of some economic weakness ahead.

Statistics Canada’s early estimate of February’s GDP growth shows no change relative to January, while tariff-related developments have the potential to significantly impact Canada’s economic growth and inflation outlook, complicating the direction of where Bank of Canada policymakers may take monetary policy next. Futures markets are currently pricing in two more 25 basis point rate reductions by the end of the year.

Europe

Frédérique Carrier – London

The EU will face steep reciprocal tariffs of 20 percent, at the top end of market fears.

U.S. President Donald Trump’s announcements are unlikely to put an end to uncertainty. RBC Capital Markets expects the EU to reserve the right to retaliate while continuing negotiations and offering some concessions, with the April 9 implementation date providing a window for further talks. U.S. policies could be revised over time, as has often been the case previously.

We continue to believe that eventually a deal will be struck, and lower, partial tariffs will end up being imposed, much like during the first Trump presidency, though this could take many months. In the meantime, the largest exporters to the U.S., including Germany and Italy, are likely to feel the brunt of tariffs on their economies. The impact on corporate earnings should be relatively contained, in our view, given many European-headquartered companies have manufacturing operations in the U.S.

From an industry perspective, automobiles are subject to a higher 25 percent tariff effective immediately, while the 25 percent tariffs on steel and aluminium announced in March remain in place. Pharmaceuticals, the single largest EU export to the U.S., copper, semiconductors, and timber are all exempt for now. RBC Capital Markets calculates that together these industries represent about a quarter of EU goods exports to the U.S., which dampens the impact of tariffs. Tariffs could be applied to these industries in future rounds, especially if the EU retaliates.

For the UK, tariffs were set at 10 percent, lower than those imposed on the EU. The UK was not a primary target of White House policies given its trade with the U.S. (imports versus exports) is roughly balanced. The UK’s failure to secure an exemption from the 25 percent tariff on foreign cars suggests that its strategy of quiet negotiations ahead of the announcement in the hope of being spared has not been entirely effective. The government has vowed to “keep a cool head” and, in our view, is unlikely to retaliate. Overall, the tariffs serve as a stark reminder that the highly sought-after free trade agreement with the U.S.—once a key goal of the Brexit agenda—remains out of reach.

With the tariff announcements larger than most observers had hoped for, both the EU and UK equity markets sold off. Retaliation risk in the EU could keep investors in the region on edge in the short term.

Asia Pacific

Jasmine Duan – Hong Kong

Asian equities declined on Thursday as concerns over U.S. President Donald Trump’s reciprocal tariffs rippled across the region’s economies. Among the regional equity markets, Vietnam saw the steepest decline, plunging 6.7 percent. The reciprocal tariff on Vietnamese goods was set at 46 percent, significantly higher than the four percent tariff that the U.S. previously had in place. Japan was the second-worst equity market performer, with its benchmark index down by around three percent.

After the imposition of a 34 percent reciprocal tariff, China now faces a total effective U.S. tariff of around 65 percent. While the tariffs are higher than many investors expected, the market reaction in China was relatively modest, in our view. The onshore CSI 300 Index declined by 0.6 percent, and the offshore Hang Seng Index fell by 1.5 percent.

The relatively restrained selloff was likely due to China’s prior preparations for such external shocks. Last week, at the China Development Forum, Chinese Premier Li Qiang stated that the government had anticipated potential external impacts exceeding expectations and was ready to introduce new policies if necessary.

What makes the situation different from the past is that China is no longer the sole target of tariffs. Other countries, especially those in Asia, are facing the same challenges.

Earnings revision trends in China are becoming more promising, with quarterly earnings for the MSCI China Index turning positive for the first time since Q2 2022. Currently, MSCI China Index companies’ direct revenue exposure to overseas markets is below 15 percent. Their revenue exposure to the U.S. is less than three percent, which is the lowest among the U.S.’s top 10 emerging market trading partners at the index level.

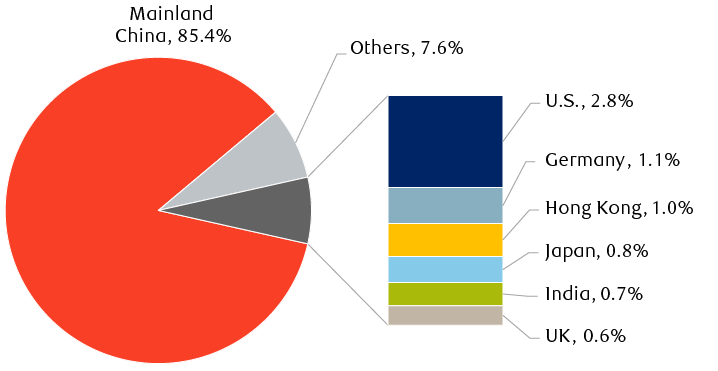

MSCI China Index companies generate 85 percent of their revenue from the domestic market

MSCI China revenue breakdown by country

The chart shows the geographic revenue breakdown of companies in the MSCI China Index. Roughly 85% of the revenue is generated from mainland China and less than 3% is from the U.S.

Source - RBC Wealth Management, Bloomberg

We think the fact that the MSCI China Index continues to trade at a discount compared to the MSCI Emerging Market Index and the MSCI Asia ex-Japan Index suggests that investors have partially factored in the tariff impact on China but not on other Asian countries.

Therefore, despite the short-term volatility, we believe Chinese equities could demonstrate resilience once the initial surprise from tariffs and any potential retaliatory measures are digested by investors.