The U.S. equity market is approaching the start of Q1 earnings season following one of the strongest five-month rallies in history. With the S&P 500 up 26.6 percent since the October low, a lot of good news has been baked in.

We think this has established a higher hurdle for Q1 earnings results, and when this happens, some high-profile companies usually stumble trying to clear the bar.

Coming together

Regardless of the Q1 earnings results and the market’s reaction, we think the full-year 2024 earnings trajectory is more important to long-term investors. And here a notable, positive shift is taking place.

The consensus forecast expects earnings growth for the technology-oriented Magnificent 7 stocks (the “haves” for over a year in terms of earnings growth and share price performance) to decline meaningfully in 2024 mainly due to very challenging year-over-year comparisons. This is not a negative development—it’s common following ultra-strong growth.

In contrast, earnings growth for non-Magnificent 7 stocks (the “have nots” for much of 2023) is expected to pick up—finally.

The two growth rates should nearly converge to around 14 percent by Q4 2024, according to Bloomberg consensus estimates, which would be well-above average.

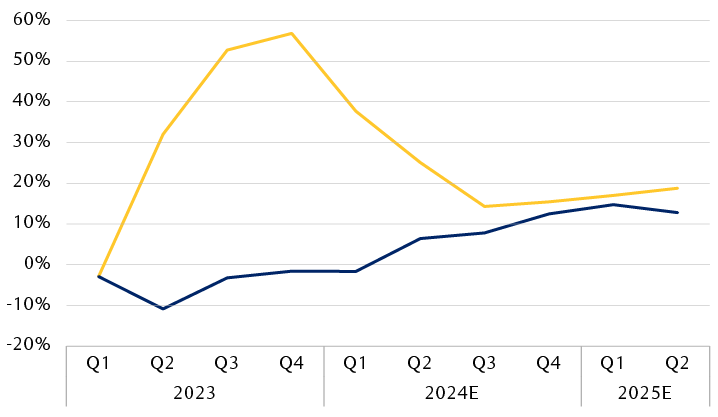

Magnificent 7 versus the rest: Earnings growth rates expected to converge

Year-over-year earnings growth and consensus estimates (%)

The line chart shows actual and consensus estimates of year-over-year earnings growth for two different segments of S&P 500: the Magnificent 7 stocks, and S&P 500 excluding the Magnificent 7 stocks. Magnificent 7 growth began Q1 2023 in slightly negative territory and rose to 56.8% in Q4 2023. Current consensus estimates are that it will decline rapidly in 2024, falling to 14.3% by Q3 2024. The consensus forecast then anticipates a gradual increase to 18.8% by Q2 2025. For the S&P 500 excluding Magnificent 7 stocks, the growth rate was also slightly negative in Q1 2023, dipped to -10.9% in Q2, and then rose, leveling off at -1.6% in Q4 2023. The consensus forecast calls for roughly flat growth in Q1 2024, followed by increases to 14.7% growth in Q1 2025, which would then be followed by a slight decline to 12.8% growth in Q2 2025. The growth forecasts for the two categories almost converge in Q4 2024 and Q1 2025.

* Magnificent 7 stocks are Apple, Microsoft, Alphabet, Amazon.com, NVIDIA, Tesla, and Meta Platforms.

Source - Bloomberg Intelligence, RBC Wealth Management; data as of 4/3/24; 2023 actual results, Q1 2024 onward Bloomberg consensus estimates (E)

This lends credence to the fact that market performance has broadened since late October 2023.

Prior to that time, the Magnificent 7 stocks within the Information Technology, Communication Services, and Consumer Discretionary sectors dominated in share price performance. These stocks and sectors rallied sharply as earnings growth prospects and results surged.

However, since the October low, five S&P 500 sectors that don’t include any Magnificent 7 stocks have climbed 17 percent or more and all 11 sectors have risen by double digits.

In other words, the market has been anticipating the earnings growth convergence between the haves and have nots, and this has been reflected by the broad rally over the past five months.

Vulnerabilities remain

When it comes to 2024 earnings estimates, the challenge is that consensus expectations are still back-end loaded. Estimates for S&P 500 earnings in the second half of the year look lofty to us.

We think the 2024 earnings growth trajectory is highly dependent on GDP growth staying resilient, near or above the 2.6 percent long-term average and without negative inflation or employment developments. While this scenario is possible, economic vulnerabilities linger, and recession risks should not be ignored.

Earnings estimates also seem to be assuming that Federal Reserve policy will turn dovish with multiple interest rate cuts.

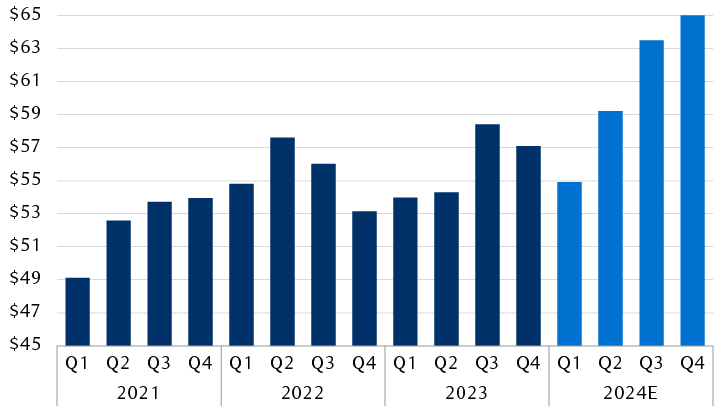

Earnings forecasts for second-half 2024 seem lofty

S&P 500 quarterly earnings per share (dark blue are actual data; light blue are consensus estimates)

The column chart shows actual quarterly earnings in U.S. dollars for the S&P 500 from Q1 2021 through Q4 2023, and the consensus quarterly earnings estimates in U.S. dollars for 2024. Earnings rose from $49.13 per share in Q1 2021 to $57.62 per share in Q2 2022. Then earnings pulled back until Q4 2022, reaching $53.15 per share. Earnings grew slightly in the following two quarters and then jumped to $58.41 per share in Q3 2023, followed by a slight dip the next quarter. In 2024, the consensus forecast is as follows: Q1, $54.92; Q2, $59.22; Q3, $63.50; Q4, $65.30.

Source - LSEG I/B/E/S, FactSet, RBC Wealth Management; data as of 3/28/24

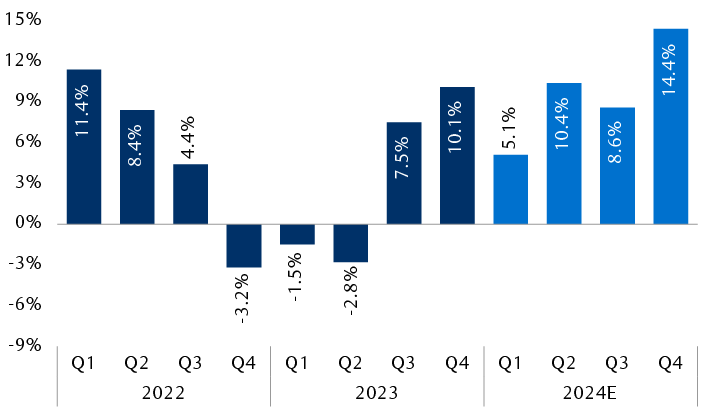

Year-over-year comparisons tougher in second-half 2024

S&P 500 earnings growth year over year (dark blue are actual data; light blue are consensus estimates)

The column chart shows year-over-year S&P 500 quarterly actual earnings growth and consensus forecasts since Q1 2022. In 2022, earnings growth rates were 11.4% in Q1, 8.4% in Q2, 4.4% in Q3, -3.2% in Q4. In 2023, it was -1.5% in Q1, -2.8% in Q2, 7.5% in Q3 and 10.1% in Q4. For 2024, the consensus forecast is for 5.1% in Q1, 10.4% in Q2, 8.6% in Q3, and 14.4% in Q4.

Source - LSEG I/B/E/S, FactSet, RBC Wealth Management; data as of 3/28/24

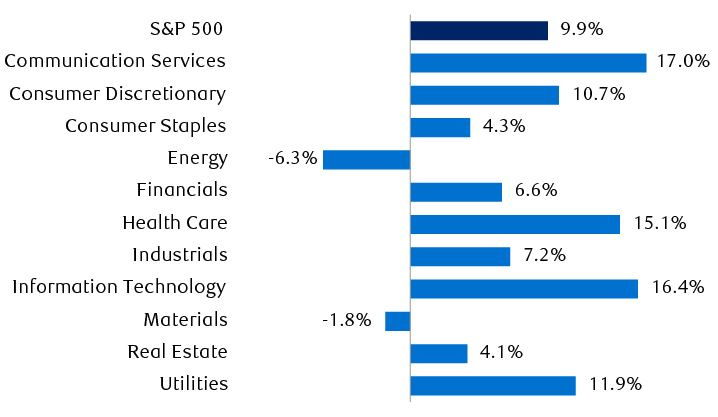

Among S&P 500 sectors, we have strong doubts that the Health Care sector will meet the 2024 consensus forecast. Earlier this week negative Medicare reimbursement rate news dented earnings prospects for managed care companies, and further estimate markdowns could occur during the Q1 reporting season. Therefore, we expect Health Care’s 15.1 percent consensus growth forecast to come down, potentially notably, given this forecast was issued just prior to the Medicare reimbursement news.

Less robust Health Care growth could be balanced out by other sectors. We think the full-year 2024 consensus growth estimates look undemanding for Financials, Industrials, Energy, and Materials; they seem achievable or beatable to us.

S&P 500 and sector consensus earnings growth estimates for full-year 2024

The bar chart shows S&P 500 and sector consensus earnings growth estimates for 2024: S&P 500, 9.9%; Communication Services, 17.0%; Consumer Discretionary, 10.7%; Consumer Staples, 4.3%; Energy, -6.3%; Financials, 6.6%; Health Care, 15.1%; Industrials, 7.2%; Information Technology, 16.4%; Materials, -1.8%; Real Estate, 4.1%; and Utilities, 11.9%.

Source - LSEG I/B/E/S, RBC Wealth Management; data as of 3/28/24

We still see scope for further market gains this year as long as the economy remains resilient, and the Fed is inclined to cut rates. But it would not be unusual for the market to take a breather or pull back at some point following such a strong run. Corrections of around 10 percent tend to happen more often than not in any given year.

We would maintain Market Weight positions in U.S. equities to balance the risks and opportunities. For more thoughts on the market, see this article.