Profit upturn

For much of the past 15 years, lackluster earnings growth has been the defining challenge for EM equities. Despite faster economic growth than developed markets, EM companies have struggled to deliver superior growth in profits and shareholder returns.

In addition to the weaker conversion of economic growth into corporate profitability, frequent equity issuances by EM companies also “diluted” per-share earnings over time. This contrasts with developed markets, where more widespread share buyback activity generally helped support per-share earnings.

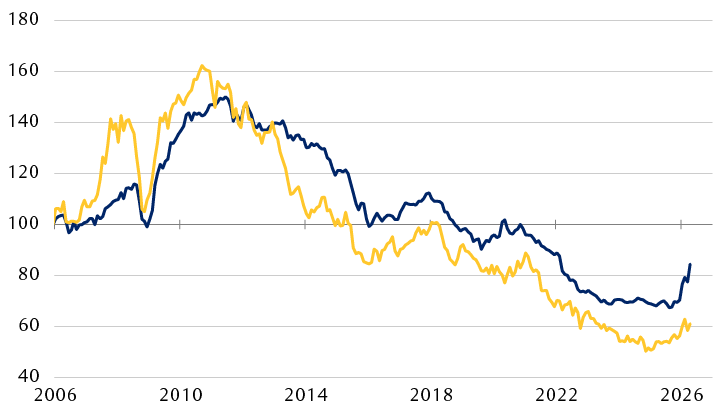

EM equities have struggled with weak growth

MSCI Emerging Markets Index vs. MSCI World Index

Indexed to Jan. 1, 2006 = 100. A rising trend implies EM is outpacing developed markets in profits and price returns, while a falling trend signals stronger earnings and returns from developed markets.

Source - RBC Wealth Management, Bloomberg; data through 4/30/26

The line chart compares the MSCI Emerging Markets Index and the MSCI World Index in terms of earnings per share (EPS) and price return from January 2006 through April 2026. Both relative EPS and relative price return rose from 2006 through 2011, indicating that emerging markets equities were outpacing developed market equities. From 2011 through 2025, both lines trended downward, indicating worse relative performance by emerging markets. Since 2025, both lines have stabilized and risen.

Recently, however, signs of improvement have emerged. EM equities have outperformed developed markets since late 2024, with the MSCI Emerging Markets Index generating annualized returns of 35.6% through April 2026 versus 17.3% for the MSCI World Index.

Encouragingly, this performance uplift has been accompanied by a stabilization in relative earnings trends rather than sentiment alone. Relative profit growth appears to have troughed in Q4 2024 and has continued to improve. After outpacing developed market earnings growth in 2024 and 2025, EM earnings are expected to maintain that lead through 2026 and 2027.

Following more than a decade of underwhelming earnings delivery, a sustained improvement in profitability could provide a firmer foundation for EM equities to maintain their upward momentum.

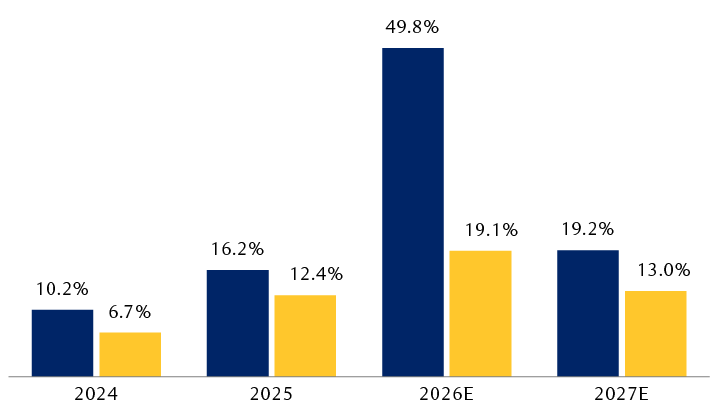

EM earnings have begun to outpace developed markets in recent years

Earnings per share (EPS) growth (y/y)

Source - RBC Wealth Management, FactSet; data through 5/22/26

The column chart shows annual earnings-per-share (EPS) growth for the MSCI Emerging Markets Index and the MSCI World Index in 2024 and 2025, and consensus estimates for 2026 and 2027. In 2024, EPS for the Emerging Markets index grew 10.2% and EPS for the World Index grew 6.7%. In 2025, the growth was 16.2% vs. 12.4%. In 2026, estimated growth is 49.8% vs. 19.1%. In 2027, estimated growth is 19.2% vs. 13.0%.

Valuation lift

Despite more upbeat profit trends and the rally over the past 18 months, EM valuations remain relatively undemanding, in our opinion. The MSCI Emerging Markets Index trades at 11.7x forward earnings, below both the 10year average of 12.2x and the 20-year average of 11.7x.

Relative valuations appear even more compelling to us. EM equities continue to trade at an exceptionally deep discount of nearly 40% relative to developed markets. While some of this discount arguably says more about elevated developed market valuations, particularly in U.S. equities, it may also signal that global investor positioning toward EM remains light after a long stretch of subdued relative performance.

In our view, periods when earnings growth improves while valuations remain discounted can create favorable conditions for better performance. If EM profitability continues to strengthen and investor confidence improves, we believe there is likely substantial room for the current sizable valuation gap to gradually narrow over time.

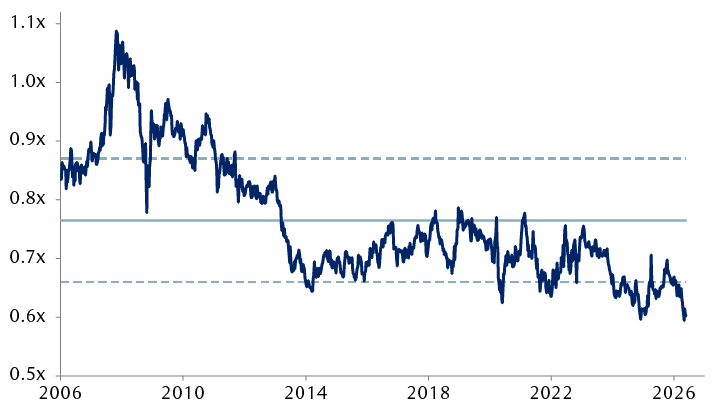

EM equities trade at a discount to global peers

MSCI Emerging Markets Index vs. MSCI World Index relative forward price-to-earnings (P/E) ratio

The MSCI Emerging Markets Index currently trades at 11.7x forward P/E, representing a 40% discount to developed markets at 19.4x, compared to a long-term average discount closer to 25%.

Source - RBC Wealth Management, Bloomberg; data through 5/22/26

The line chart shows the forward price-to-earnings (P/E) ratio of the MSCI Emerging Markets Index relative to the MSCI World Index from January 2006 through May 22, 2026. The average over this period was roughly 0.76x, with a one standard deviation band between 0.65x and 0.86x. From 2006 through the end of 2010, the relative P/E ratio was mostly more than 1 standard deviation above the average. It then declined to roughly 0.65x in 2014 and remained in a range between roughly 0.65 and 0.76 until early 2024. Since then it has trended moderately lower.

Macro foundation

Some of the skepticism toward EM assets can be traced back to concerns about macroeconomic instability. These risks will likely linger, in our opinion, but it is worth noting that many EM countries have made considerable progress bolstering economic resilience with policy reforms in recent years.

Central banks’ credibility has improved, reliance on foreign-currency debt has declined, and corporate governance initiatives have accelerated and become more shareholder-oriented across many EM countries.

These structural improvements may help explain why EM equity volatility has moderated in recent years. Between 1988 and 2020, the rolling 12-month price return volatility for the MSCI Emerging Markets Index averaged 20.8%, compared with 13.7% for developed markets. Since 2020, however, EM volatility has averaged 16.5%, much closer to the 15.9% average for developed markets.

A better setup ahead

Over time, equity markets tend to follow the direction of earnings. Given EM cycles have historically unfolded over multiyear horizons, we believe the recent inflection in relative profit trends warrants monitoring as it may represent the early stages of a more durable shift in trend.

Currency dynamics may also become increasingly supportive if the U.S. dollar transitions into a weaker phase after an extended period of strength. Historically, weaker U.S. dollar environments have tended to coincide with improved performance for EM assets.

Meanwhile, EM equities could also benefit from renewed portfolio reallocation flows seeking diversification and growth at less-expensive valuations. In addition, the composition of the EM equity universe has evolved meaningfully over time. Tech-related sectors now account for a larger share of the MSCI Emerging Markets Index, providing investors with alternative ways to participate in the global AI ecosystem beyond the dominant U.S. market.

The convergence of improving corporate fundamentals, stronger macro foundations, undemanding valuations, and relatively conservative investor positioning suggests to us that the longer-term setup for EM equity performance has become more constructive.