What was widely expected to be a rather uneventful first Federal Reserve meeting of the year proved to be anything but. Though heightened market volatility around it may have been amplified by other events this week, the Fed’s relative reluctance to formally open the rate cut window sparked some interesting market reactions.

While most would probably argue that the Fed was a bit late to the rate hike party in 2022, the underlying risk for markets—and the economy—is that it could also be late to the rate cut party. To be sure, Powell this week acknowledged the risks of cutting too late, especially as inflationary pressures have receded more rapidly than policymakers had expected late last year. But the market reaction this week suggests that risk remains—if not even more elevated.

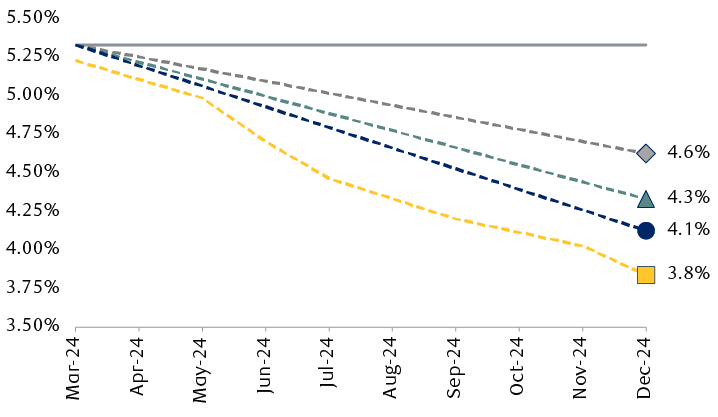

Powell’s comments were successful in culling market pricing of a March rate cut with probabilities fading to roughly 30 percent from a peak closer to 90 percent in January. But markets simply took that and ran with the idea that a later start to rate cuts might only mean that a greater number of cuts are ultimately needed. Prior to Powell’s comments, markets were pricing in about five 25 basis point rate cuts to around 4.1 percent by the end of the year; now markets are pricing deeper cuts to around 3.8 percent.

And this dynamic is pressuring Treasury yields lower. The benchmark 10-year Treasury note yield has faded to just 3.8 percent (in line with rate cut expectations) from a 2024 peak of 4.2 percent achieved one week ago, and notably down from the 2023 high of five percent. A break below 3.8 percent would mark the lowest level since this past July.

When rate cuts start doesn’t matter; where rates end up does

The line chart shows the expected level of the U.S. federal funds rate, relative to the current 5.3%, in the fourth quarter of 2024, according to four sources: the Federal Reserve’s own projection (4.6%), Bloomberg consensus (4.3%), RBC Capital Markets (4.1%), and the projection based on current market pricing (3.8%).

Source - RBC Wealth Management, Bloomberg; data as of 2/1/24, forecasts shown for Q4 2024

Ghosts of banking stress past

We would be the first to concede that getting a clean read on the market’s interpretation of the Fed meeting this week was certainly clouded by market stress elsewhere. Specifically within regional banks as New York Community Bancorp’s (NYCB’s) stock price fell by half following its Q1 earnings report where the dividend was cut by 70%.

A drop of that magnitude sparked broader selling pressures within the regional banking sector, raising investor concerns that the ghosts of banking stress that visited markets last spring could be coming back to haunt again.

However, our early read is that this is a localized event and not a harbinger of another round of broader regional banking stress on par with what markets weathered last year. RBC Capital Markets analysts noted: “Results had several negative surprises, including a higher-than-expected provision and reserve build, a meaningfully lower margin and outlook, and a dividend cut announcement. We believe that many of these trends are related to the company crossing the $100 billion asset mark and becoming a Category IV financial institution, which is driving increased liquidity and compliance needs, though in aggregate the results were less than expected. The 2024 outlook also suggests some further margin and expense pressures due to these themes.”

The confidence game

Turning back to the Fed and where things might go from here, we think inflation is still the name of the game. This is perhaps also where the greatest disconnect between Powell’s comments and current market sentiment lies.

We think the clear takeaway is that the Fed still wants even more evidence, and greater confidence, that inflation is on a firm path back to two percent. In our view, it is. Core Personal Consumption Expenditures Inflation (excluding food & energy) has been running below the Fed’s two percent target over the past three and six months, at 1.5 percent and 1.9 percent annualized, respectively. While Powell somewhat dismissed those numbers and fell back to highlighting the year-over-year pace at a still-elevated 2.9 percent, we do think the Fed is closer to the point of declaring victory than policymakers are letting on. We remain highly certain the Fed won’t wait until annual inflation is back to two percent, as by then it would be far too late. Markets perhaps just wanted more acknowledgment of recent inflation progress.

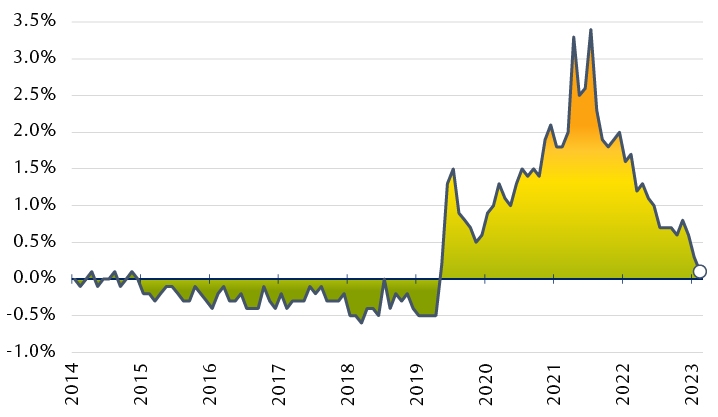

Other data released this week showed another sharp drop in consumer inflation expectations. As shown in the last chart, one-year inflation views have almost unwound all of the rise over the past two years, and are now in line with historically standard levels.

Consumer inflation expectations are essentially back to normal

Deviation of consumer expectations from 2014–2024 median

The line chart shows, for the period of 2014 to January 2024, the deviation of consumer inflation expectations over a one-year time horizon from the median level over that period. The deviation was largely negative by 0.5% or less until mid-2020, when it suddenly rose to 1.5% above the median. Consumer expectations reached a maximum of almost 3.5% in mid-2022, and have since trended downward to 0.1% in January 2023.

Source - RBC Wealth Management, Bloomberg, Conference Board Consumer Confidence Survey; monthly data, 12/31/14–1/31/24

The Fed’s goal of approaching the “highly consequential” decision to begin cutting rates “methodically and carefully,” as various policymakers have recently suggested, may seem prudent on the surface, we—and the market—clearly want a more deft and flexible approach if the Fed is going to pull off a soft landing for the economy. We think the Fed will get there, even if it has stumbled out of the gate.

We think there is 50 percent chance a March rate cut will occur based on the incoming data, but, at a minimum, the meeting will likely set the stage for a May cut, with more to follow this year.