The Memorandum of Understanding (MoU) reduces the risks of conflict-driven economic weakness and market volatility, in our opinion. The truce, however, remains precarious. We explore the macroeconomic implications of the MoU and the strategic priority it leaves untouched for governments and corporates alike—the drive towards self-sufficiency.

Strait talk

The MoU signals the cessation of hostilities, and includes an agreement to open the Strait of Hormuz, and the start of negotiations. The agreement is fragile, however, as many questions remain unresolved, including the contentious issue of Iran’s nuclear capability, the very matter which started the war in February.

In the Global Insight 2026 Midyear Outlook, we noted that the path of the global economy and financial markets depended on the Strait’s reopening and how quickly energy and commodities flows would be normalized.

Most observers maintain that the full reopening of the Strait and normalization of flows will be fraught with difficulty. The scale of the backlog, with some 600 vessels trapped in the Persian Gulf, and the alleged presence of mines present significant challenges. Indeed, RBC Capital Markets, LLC’s Head of Global Commodity Strategy and Middle East and North Africa (MENA) Research Helima Croft sees multiple reasons to view the agreement circumspectly.

RBC Global Asset Management Inc. Chief Economist Eric Lascelles takes a more constructive view. He notes that while official data shows that commercial traffic through the Strait has stalled since the beginning of the war, satellite data from our third-party research provider suggests a shadow fleet—vessels operating with their transponders turned off—went undetected by traditional trackers even before the MoU was signed. This may explain why the prediction markets are cautiously optimistic about the formal reopening.

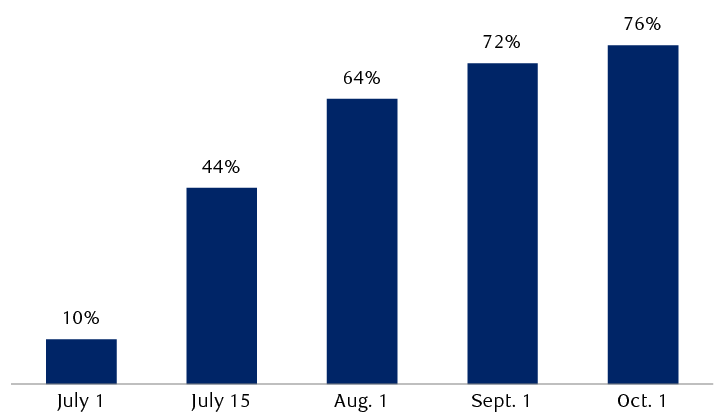

Prediction markets are cautiously optimistic for a return to normal in the Strait of Hormuz

Kalshi odds of traffic normalization by a given date

As of June 25, 2026, 10:00 CDT. Normalization is defined as a seven-day moving average of at least 60 vessel transits per day, or roughly two-thirds of the 90–100 ships that passed through the Strait of Hormuz daily before the conflict.

Source - RBC Wealth Management, Kalshi

The chart shows the chances of ship traffic through the Strait of Hormuz returning to normal by a series of dates, according to the Kalshi prediction market, as of July 25, 2026, 10:00 CDT. The odds are 10% by July 1, 2026, 44% by July 15, 64% by August 1, 72% by September 1, and 76% by October 1.

Improved economic outlook

A lasting truce could have important implications for inflation, interest rates, and growth.

Oil prices have already corrected to close to $74.00 per barrel, more than one-third less than their March peak, though still slightly above pre-war levels. Natural gas prices have fallen similarly, yet remain some 33 percent above pre-war levels in Europe. In the U.S., average national gasoline prices are falling closer to $4.00 per gallon.

The fall in energy prices from their peak does not mean the inflation shock is over. Jet fuel inflation may edge up further before inventories are replenished, even as U.S. gasoline price inflation has likely peaked. In Europe, energy bills are often indexed to natural gas with a lag, which will likely push inflation up over the coming months. Other commodities may yet feel a lagged effect of the war.

Moreover, with energy prices still above pre-war levels, inflation may still rise modestly in the near term. However, the spike looks set to be shorter-lived than markets had anticipated before the truce.

Overall, developed market central banks such as the European Central Bank and the Bank of England that were considering tightening monetary policy in response to energy-driven inflation, may face less pressure to do so. By contrast, those operating in stronger cyclical conditions with tight labour markets, such as the Federal Reserve and the Bank of Japan, may well consider raising rates despite inflation waning.

If negotiations remain on track and the Strait stays open, we believe the global economy is likely to regain its pre-war momentum by the autumn. For Asia and Europe, the two regions most affected by the disruption to Middle East energy flows, the truce comes as a particular relief.

Self-sufficiency in a multipolar world

Even if negotiations prove successful and peace endures, we expect governments and the corporate sector to remain focused on improving self-sufficiency to navigate the increasing uncertainties of a multipolar world order.

We think many countries will be increasingly wary of depending on Middle East energy flows. We expect this to accelerate investment in diverse energy sources including nuclear and renewables, as well as in power grid infrastructure .

The Middle East conflict has equally reinforced the importance of national defence spending. In our view, governments will not only sustain elevated defence budgets, but increasingly direct them towards modern precision capabilities: offensive strike drones and hypersonic missiles, drone and missile defence complexes, and AI-integrated systems. For Europe in particular, the conflict has accelerated the push for strategic autonomy, reducing dependence on U.S. security guarantees.

For the corporate sector, the U.S.-Iran conflict has reinforced the increased importance of inventory buffers and financial hedges. RBC Capital Markets, LLC’s Head of U.S. Equity Strategy Lori Calvasina partly ascribes the strength of Q1 2026 U.S. corporate results to companies having taken these steps in advance. Management teams have absorbed the lessons of COVID-19 and abrupt shifts in U.S. tariffs. Companies have replaced “just in time” supply chain management—or minimizing inventory to reduce costs—with a “just in case” approach, prioritizing resilience over efficiency. We expect them to maintain this approach.

An unstable truce

The MoU is a meaningful step back from the brink, but it falls well short of a lasting settlement.

Markets have nonetheless initially responded with cautious optimism. Global bond yields have eased marginally as inflation fears have receded. Stock markets exhaled, suggesting to us that despite their recent strength, the conflict had weighed on sentiment. A successful and lasting agreement could unlock further upside potential, though a breakdown in talks would likely reverse these gains.

Regardless of the outcome, we think the structural priority that defined the pre-war landscape—the drive towards self-sufficiency—remains firmly in place.