As was widely expected, the Fed delivered its third consecutive rate cut to close out 2025, while remaining noncommittal on what investors might expect into 2026. But we believe this latest cut could mark an inflection point for policy, the economy, and markets.

With this latest rate cut to an effective midpoint of 3.63 percent, and after a multiyear campaign of elevated levels, policy rates now appear to be within the theoretical “neutral” range for the U.S. economy—or the estimated point at which monetary policy is neither restrictive nor supportive of economic growth and inflationary pressures. At the December meeting, policymakers judged the range to be from 2.6 percent to 3.9 percent, with a median of 3.0 percent.

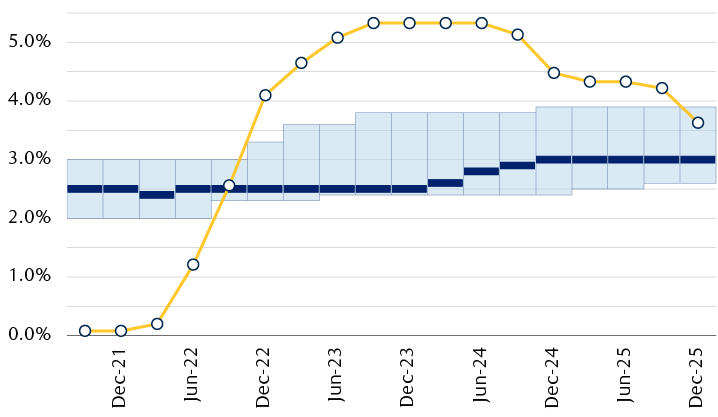

U.S. interest rates enter the “neutral” zone

Source - RBC Wealth Management, Bloomberg, Federal Reserve; shows median and range of longer-run fed funds projections

The chart shows the midpoint of the Fed's policy rate relative to the Fed's quarterly projections of the longer run interest rate, or the neutral. In December, the range of estimates spanned form 2.6% to 3.9%, with a median of 3.0%. With policy rates now at 3.63%, rates have fallen within the upper bound of that range.

While unchanged, both the median and the range have been trending higher in recent years from pandemic-type levels. And with nearly half the policymakers believing the so-called neutral rate is above 3.0 percent, any further cuts would cause more to see policy as moving into easy territory at a time when the economic and inflationary backdrop might not necessitate it.

Impulse control

But with the Fed taking its first steps down easy street, is it at risk of a head-on collision with something unexpected?

The Fed made several notable adjustments to its summary of economic projections. Economic growth for next year was upgraded sharply to 2.3 percent from just 1.8 percent in September. A 2.3 percent pace would also be well above the Fed’s 1.8 percent estimate of the long-term sustainable growth rate for the U.S. economy—something that would normally add to inflationary impulses.

But perhaps not so, at least in the eyes of the Fed. Expected core personal consumption expenditures inflation for next year was lowered slightly to 2.5 percent from 2.6 percent in September, though also still well above the Fed’s 2.0 percent inflation target (in fact, the Fed’s latest projections don’t have inflation returning to 2.0 percent until 2028). When pressed on why stronger growth next year was paired with a lower inflation forecast, Fed Chair Jerome Powell alluded to the idea that AI and productivity gains could help to offset inflationary pressures. While possible, technology-driven productivity gains can be fleeting, while taking years to fully understand and realize.

Finally, unemployment is seen ending 2026 at 4.4 percent, unchanged from the Fed’s prior estimate, and in line with the current unemployment rate. Again, that’s at odds with a stronger growth backdrop, but this too could be reflective of AI as labor markets face a technology-driven transition and inflection point.

That said, we are flagging signs of an improving labor backdrop in recent months. This week, job openings through October were much higher than Bloomberg consensus expectations, and now appear largely unchanged over the past year, still at historically high levels. At the same time, 19 percent of small businesses reported plans to hire, matching the best reading since 2022. Though intentions to hire can be volatile, this does square with other recent measures of consumer sentiment such as the Conference Board’s survey of whether jobs are perceived as “hard to get,” which fell to the lowest level since June, and the University of Michigan’s survey of job loss probability, which fell sharply in the first part of December.

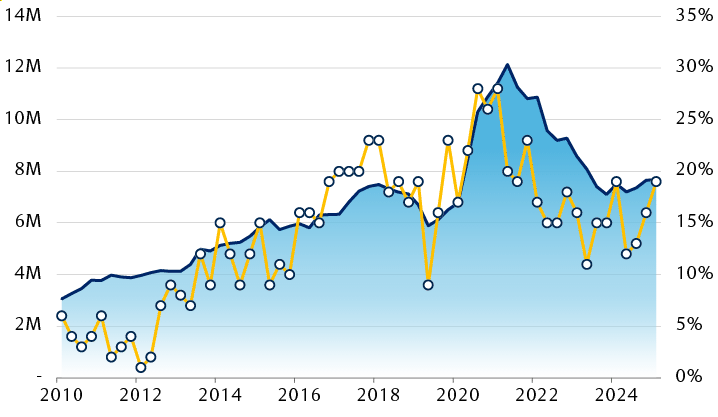

U.S. labor market showing signs of life?

Source - RBC Wealth Management, Bloomberg, NFIB Small Business Survey

The chart shows the number of U.S. job openings and the net percentage of small businesses surveyed by the NFIB that intended to hire over the next three months. There were 7.6 million job openings as of October 2025, which is in line with the average of the past two years. At the same time, 19% of small businesses reported plans to hire over the next three months, matching the highest level observed since 2023.

All told, we see upside risks to economic growth and to some extent inflation next year, while we think recent Fed action will be sufficient to shore up labor markets with potential for another hiring rebound, just as we saw in early 2025.

When 2 = 6

The other focal point of the meeting was on the extent to which policymakers might dissent, either in favor of a cut if the Fed held rates steady, or in favor of doing nothing if it cut. In the end, just two policymakers voted against this week’s rate cut.

However, looking at the Fed’s updated rate projections, six policymakers penciled in rates ending this year at an upper bound of 4.0 percent, implying no further rate cut at the December meeting this week. Perhaps none of those people vote on policy this year, or perhaps Powell was simply able to wrangle others into supporting a rate cut. But that suggests there’s already a large cohort at the Fed that still foresees a strong case to keep rates steady.

The composition of voters next year will also tilt more hawkish, in our view, with two of the most hawkish members at the Fed based on public comments, the presidents of the Dallas and Cleveland Federal Reserve Banks, joining the voting rotation, along with the Minneapolis Fed president who has also been vocal about being cautious with respect to further rate cuts.

Regardless, the stage is set for next year—and a new Fed chair—and what will likely be a continuation of contentious Fed decisions. It may also mean more volatility and uncertainty as the power at the Fed may shift from the chair to the voting committee, with markets more attuned than usual to public comments beyond the Fed chair.

What does it all mean?

With respect to Treasury yields, and the shape of yield curves, we think moderately higher and slightly steeper is the near-term trend. With the Fed on hold, though biased toward another cut, the 2-year Treasury yield is likely to remain around 3.5 percent. But the 10-year yield, which is more sensitive to economic growth and inflation, likely faces further upside risk from a current level around 4.10 percent. In our view, if labor markets stabilize and/or reaccelerate, we see scope for it to move back into a range of 4.2 percent to 4.6 percent, where it was prior to September.

For fixed income investors, we believe this will remain an attractive environment to take advantage of steep yield curves and any backup in yields to reposition portfolios by exiting shorter-dated bonds in favor of locking in higher yields and for a longer time further out on curves.

For markets broadly, the Fed now joins an ever-growing number of global central banks that are at or near the end of their respective rate cut cycles, with some even turning the page toward the potential of higher rates—and an associated turn toward a more volatile market backdrop.