As fate would have it, on this day eight years ago Jerome Powell was sworn in as the 16th chair of the Board of Governors of the Federal Reserve, dating back to 1914. For perspective, there have been 20 different U.S. presidents over the same stretch.

Clearly then, a new Fed chair is no insignificant occasion. But for all the drama around it, up to and including the pick of former Fed Governor Kevin Warsh to take over from Powell, is it really all that significant this time around?

Getting to know you

By way of short introduction, following a relatively short stint on Wall Street, Warsh made the jump to the White House in 2002 via an economic advisory role, before famously becoming the youngest Fed governor in history in 2006—which unceremoniously ended with his resignation in 2011 largely in protest of the central bank’s quantitative easing program. (More on that in a moment.)

As has been widely covered by the media, Warsh’s reputation is largely that of a traditional “hard money hawk,” which naturally has raised eyebrows given Trump’s very public—and unambiguous—desire to see interest rates lowered. Of course, views change, but since leaving the Fed in 2011 there’s simply little evidence to believe they have, in our view. While we think it’s safe to say Warsh wouldn’t have gotten the nod had he not voiced agreement with lower rates, Trump alluded to the reality that talking the talk is one thing, walking it is usually another, lamenting at the recent World Economic Forum in Davos that officials tend to “change once they get the job.”

All told, it’s a fine choice, even if we don’t find it a particularly inspired one. Beyond that, we think the market reaction—to the limited degree we can explicitly tie it back to this choice—likely is the exact opposite of what the administration hoped to see.

Judgment day

It has been nearly a week since the initial reports that Trump had zeroed in on Warsh as his pick. And while it’s never so easy to explain market dynamics via a singular lens, it does appear to us that the one-two combo of a Fed rate cut pause and a more hawkish-than-expected choice to replace Powell last week at a minimum kicked off this recent bout of market volatility and sector rotation.

Since last Tuesday, Bitcoin has declined more than 25 percent; gold is down sharply, the dollar has rallied nearly two percent; the S&P 500 has dropped to the lowest level since last December led by Tech and software—all generally the opposite of what one would expect if Fed sentiment was seen as shifting more dovish with someone new at the helm. But market expectations for Fed rate cuts over the near- and long-terms are essentially unchanged—the market-implied prospect of a cut at the Fed’s June meeting is still barely 50 percent, while markets are still fully priced for roughly 50 basis points (bps) of cuts in total this year—a far cry from the president’s stated aim of rates being lowered by 200–300 bps.

Again, recent market rallies in certain corners of the market amid a confluence of factors left some asset classes at potentially lofty valuations, but sometimes all it takes is a spark. The other possibility, in our view, is that where questions remain about where Warsh’s interest rate conviction lies, there’s one area where his beliefs have remained consistent.

Is this elephant with us in the room right now?

In a 2025 speech, Warsh perhaps laid out his broader ethos of the Fed, and where he may aim to leave his mark—the Fed’s balance sheet and what he perceives to be the Fed’s “mission creep” away from its traditional congressional mandates of price stability and maximum employment.

For nearly 20 years now, the Fed’s balance sheet has been the elephant in the room for markets, and to some extent, the U.S. Congress. But via both purposeful, and natural, efforts—the elephant simply isn’t what it used to be. In absolute terms, the Fed’s balance sheet is still north of $6 trillion, but that is now just around 20 percent of U.S. GDP, and only 11 percent of the market capitalization of the S&P 500, from peaks of closer to 35 percent and 30 percent, respectively. The Fed’s footprint is already smaller than many might believe.

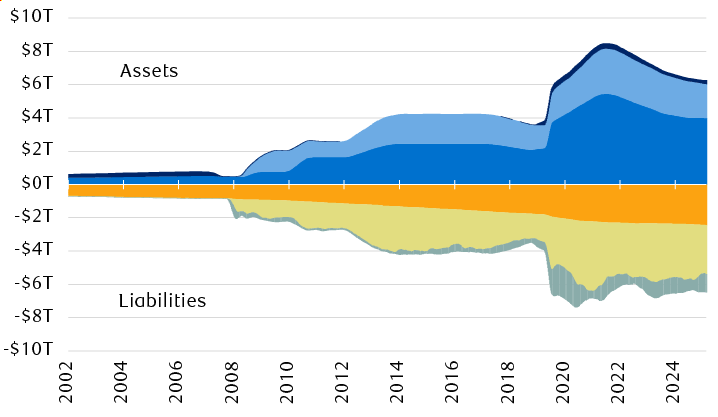

And it’s smaller still when we think about the drivers of its expansion. The chart shows a basic view of the Fed’s assets and liabilities. Two liabilities it has are the currency in circulation, now at roughly $2.5 trillion, and the cash the Treasury Department holds at the Fed in its general account, about $900 billion. The Fed controls neither of those things. And no, the Fed doesn’t “print money”; currency outstanding is simply a function of economic growth and the demand for it via the banking system.

Breaking down the Fed’s balance sheet

USD trillions

Source - RBC Wealth Management, Bloomberg; assets do not equal liabilities due to the exclusion of some smaller components for simplicity

The chart shows the primary assets and liabilities on the U.S. Federal Reserve’s balance sheet. Both assets and liabilities increased after the 2008 financial crisis and again during the COVID-19 pandemic in 2020. Assets are T-bills, mortgage-backed securities, and Treasury securities. Liabilities are currency in circulation, bank reserve balances, and the Treasury General Account. Total assets rose to more than $8 trillion in 2022 and have since declined to roughly $6 trillion. Liabilities reached more than $7 trillion in 2021 and are currently near $6 trillion.

At a minimum then, and through no fault of its own, the Fed’s balance sheet would have to be at least roughly $3.5 trillion. The balance then is bank reserves, or the regulatory capital banks are required to have, at about $3 trillion. There could be regulatory relief to bring that number down. Against all of that, the Fed holds a mix of Treasuries and mortgages as assets. With limited room to shrink the balance sheet, Warsh could lead a drive to simplify it instead, by either selling mortgages and/or by shortening the maturity of Treasuries. But in our view, that could drive longer-term bond yields and mortgage rates higher—at odds with the administration’s aim of bringing borrowing rates lower.

Markets, rightly or wrongly, might be concerned about Fed balance sheet issues. But just as interest rates are set by the Federal Open Market Committee (FOMC), so too are balance sheet decisions—and we see no reason to believe that the core of the FOMC will see the need to change course under a new Fed chair. Still, this appears to us to be one risk factor that markets might be homing in on.

New Fed chair, same old problems?

Our view had been that regardless of who replaced Powell, the power within the FOMC was likely to shift to the voting members and away from the chair, simply from the nature of the process thus far. Policy decisions will still be made prudently and based on the economic data by a majority—but likely with more dissents at times.

One risk we see is what happens if the Fed opts not to cut rates at the June meeting when Warsh will take over if confirmed. What if there are only modest cuts this year, if any at all? Will Trump ramp up his criticism and risk further market volatility and further Fed independence fears? Could he try to replace Warsh?

Ultimately though, we think it’s still business as usual. There’s no free lunch, and no easy path to lower rates for the sake of lower rates. Fed decisions this year will be determined based on the incoming data, but as a new Fed chair is a relative rarity through history, it will almost certainly come with its own uncertainty for markets to navigate.