Chinese equities closed out 2025 with strong annual gains for the second consecutive year. The MSCI China Index surged 31 percent, while Hong Kong’s benchmark Hang Seng Index rallied 28 percent. The gains caught many market participants by surprise, as numerous analysts had urged caution at the start of 2025 due to ongoing U.S.-China trade tensions.

We think the following factors will shape equity market returns in 2026.

How will policymakers set the economic growth target?

Chinese policymakers outlined their roadmap for 2026–2030 in the 15th Five-Year Plan announced in October 2025. Regarding economic growth, the plan aims for China to reach the level of moderately developed countries by 2035. This implies nearly a 50 percent increase in GDP per capita to US$20,000 from the current US$13,300 level.

Policymakers specified that China will achieve an annual average economic growth rate of 4.17 percent over the next decade in official Party study material. While the 2026 GDP growth target is expected to be officially announced in March, we anticipate the growth rate will remain elevated (i.e., around five percent) in the coming years before gradually moderating.

Securing higher growth at the outset of the 15th Five-Year Plan period would allow the target to ease in subsequent years, in our view. Pursuing stronger growth in the early phase may also be a positive indication, bolstering household and business confidence.

But what about long-term growth challenges?

Setting ambitious growth targets is inspiring, yet investors may question their achievability. Many market participants argue that China continues to face multiple long-term growth challenges, for example, an incomplete property market correction, weak domestic consumption, deflationary pressures, and persistent geopolitical tensions. While these issues are unlikely to resolve quickly, their broader economic and equity market impacts require careful analysis, in our view.

Take the property sector as an example. Residential property prices and investment remain in a downturn, and developers continue to face distress. Notably, two-thirds of China’s top 50 developers have defaulted on bond payments in recent years.

However, the impact on the economy and equity market should be less severe than years ago. At the peak in 2018, property and related sectors contributed 25 percent of China’s GDP, but Bloomberg Economics estimates suggest this share has fallen significantly, and the economic contribution from technology industries has filled the property sector’s shoes. The property sector now accounts for just 1.4 percent of the MSCI China Index, limiting its direct equity market impact even if negative news from developers continues to emerge.

The housing market correction no longer poses systematic financial risk, in our assessment. Policymakers have reduced emphasis on the property sector, ranking it last among eight economic priorities for 2026.

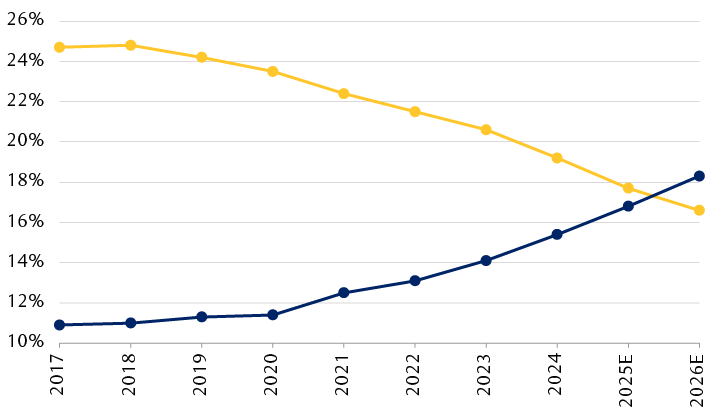

China’s economic contributions from technology industries have filled the property sector’s shoes

Technology-related and property-related sectors’ contribution to Chinese GDP

Source - RBC Wealth Management, Bloomberg Economics, National Bureau of Statistics of China; figures for 2025 and 2026 represent Bloomberg Economics projections.

The chart shows contributions to Chinese GDP by technology-related and property-related sectors annually since 2017, with Bloomberg Economics projections for 2025 and 2026. At the peak in 2018, property and related sectors contributed around 25 percent of China’s GDP, but this share has fallen significantly. It’s contribution is estimated to be 16.6 percent in 2026. For technology-related sectors, the contribution to GDP is projected to increase to 18.3 percent in 2026, from roughly 11 percent in 2018.

Shifting means of boosting domestic demand

The 15th Five-Year Plan prioritizes domestic demand and consumption more than ever. However, recent stimulus measures—such as the revised trade-in subsidy program for consumer goods—suggest to us that subsidy amounts and scope in 2026 will be more restrained than last year. This raises the question: Is boosting domestic demand merely a slogan, or will the government implement meaningful action?

We believe the approach to supporting domestic demand has shifted. Policymakers are now focusing on reducing income inequality and preventing a resurgence in rural poverty. Recent labor market weakness has suppressed wage growth for migrant workers, and the growth in migrant worker numbers has slowed significantly since 2023. The rural poverty rate could increase if migrant workers lose their jobs in the city and move back to rural areas.

Therefore, we anticipate more targeted measures aimed at redistributing and strengthening the social safety net for lower-income groups, rather than broad-based consumer subsidies. Potential new initiatives, such as reducing maternity-related costs, may also be introduced.

Technology transcends self-sufficiency to emerge as a growth driver

It is unsurprising that policymakers have prioritized advancing science and technology and industrial modernization as the top goals for the next five years. However, the technology agenda extends beyond national security and self-sufficiency.

Following recent breakthroughs in electric vehicles, innovative drugs, and AI, technology has emerged as a new driver of China’s economic growth. Policymakers aim to deploy technology economy-wide to enhance productivity, enable scalable commercial applications, and generate new demand.

China is making rapid progress in technological adoption, leveraging its manufacturing supply chain advantages. For instance, its deployment of robotics in manufacturing is 12 times greater than the U.S. when adjusted for income.

To achieve these goals, we think the central government may assume a greater role in directing technology and industrial policy. This could reduce local protectionism, market segmentation, and overcapacity issues.

Renminbi appreciation

The renminbi has begun 2026 with a notable rally, appreciating nearly one percent against the U.S. dollar over the past month and strengthening past CNY 7.0 for the first time since 2023.

We believe the People’s Bank of China may tolerate further renminbi appreciation against the dollar as the U.S.-China trade truce looks more durable this time. If growth concerns ease and depreciation risks subside, we think the central bank is likely to reduce currency market intervention, consistent with historical patterns.

Implications for the equity market

After a year dominated by U.S.-China trade tensions, China’s economic trajectory appears to be back under its own control. The latest trade deal between the two countries, reached in October, appears more durable and is likely to set the stage for a more sustainable Chinese equity market rally, in our view.

Following a pullback in Q4 2025, the MSCI China Index trades at a more reasonable valuation, with a 12-month forward price-to-earnings multiple of 12.7x, slightly above an 11.6x historical average. Notably, valuations of China’s AI and internet leaders still look discounted relative to their U.S. peers. As investors increasingly question whether U.S. AI companies are overvalued, we anticipate greater interest in Chinese AI stocks. This could provide support for the broader equity market.

With the contribution of Leo Shao.