A case of whiplash? Many investors are likely experiencing whiplash following a dramatic U-turn in equity markets as the S&P 500 surged 13 percent over the past few weeks following a 10 percent correction in Q1 2026.

Short-term indicators are overbought. With near-term technical indicators tracking two-to-four-week swings now back to overbought territory – signaling a pending pause or pullback – investors are understandably questioning whether the rebound is sustainable.

Two technical reasons suggest further upside. While valuations, the war in Iran and its effect on inflation, and global growth remain ongoing fundamental concerns, we see two technical reasons to remain cautiously optimistic moving through Q2 2026.

First, participation remains positive. Breadth of participation, as measured by advance-decline lines, remains positive with the S&P 500 and NYSE advance-decline lines at or near new highs. As a general rule of thumb, equity cycles don’t usually peak when participation is broad with advance-decline lines at or near all-time highs.

Second, the largest sector in the market, Technology, is accelerating following a Q4 2025–Q1 2026 correction. More importantly, with the Information Technology (35 percent) and Communication Services (12 percent) sectors accounting for just under 50 percent of the S&P 500’s market capitalization, their direction will define the overall trend of the S&P 500.

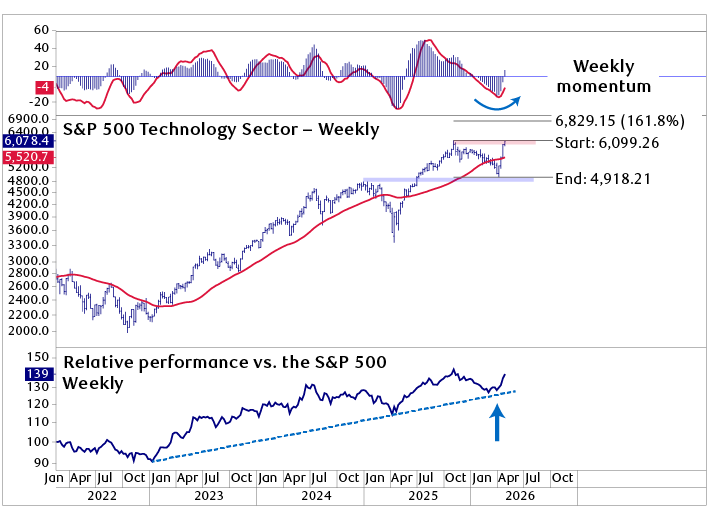

S&P 500 Information Technology sector with weekly momentum, a 200-day moving average and relative performance versus the S&P 500

Source - RBC Wealth Management, Bloomberg, Optuma

This chart illustrates the performance of the S&P 500 Information Technology sector from March 2022 through April 22, 2026. The top panel shows weekly price momentum, indicating it is currently early in an upturn. The middle panel shows the sector price, indicating a volatile but upward slowing trend defined by a series of higher highs and higher lows. The bottom panel shows the relative performance of the sector versus the S&P 500 as a whole, with a pullback from the fourth quarter of 2025 through the first quarter of 2026 now bottoming and rising relative to an uptrend line that started in the fourth quarter of 2022.

Weekly momentum has bottomed and turned up for Technology. The first technical observation we highlight is that the weekly momentum indicators have turned up from oversold levels, which developed through Q4 2025 and into late Q1 2026 as growth stocks sold off. We focused on this indicator in the Feb. 26 Global Insight Weekly as a potential catalyst for a rotation back to growth stocks. With that indicator now early in an upturn, we expect further upside through the quarter.

Technology’s uptrend is intact. Secondly, although the Technology sector’s price has surged back to resistance at the Q1 2026 highs – where a near-term pause is likely – the overall trend of higher lows and higher highs remains intact. A breakout above 6,100 would be supportive of further upside to the 162 percent extension level near 6,800 numbers.

Relative trend remains positive. Lastly, and arguably most importantly, the overall trend of the Technology sector’s relative performance versus the S&P 500 remains intact with the Q4 2025–Q1 2026 pullback bottoming at the uptrend line. Put differently, until that uptrend shows evidence of turning negative, we would caution investors against turning overly bearish on the sector.

Interest rates

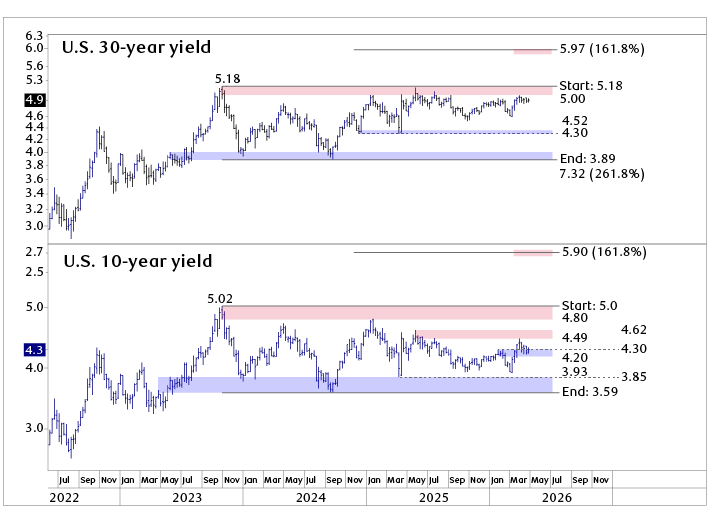

Range-bound despite an ongoing war. While equity markets have rebounded from oversold levels at the end of Q1, the direction of interest rates will continue to be an important catalyst for equities. The U.S. 30-year and 10-year Treasury yields illustrate that despite the war in Iran – and potential risk to supply chains and inflation – long-term interest rates remain in relatively narrow sideways trading ranges that began in Q4 2023.

U.S. 30-year and 10-year Treasury yields remain range-bound below important technical levels

Source - RBC Wealth Management, Bloomberg, Optuma

This chart illustrates the yields on the 30-year and 10-year U.S. Treasury bonds from September 2022 through April 22, 2026. After moving higher from their 2020 lows, both long-term U.S. Treasury yields peaked near 5% in the fourth quarter of 2023 and have since traded sideways in narrow range between 3.5% and 5%.

Technical levels that matter. We highlighted in red and blue the upper and lower bands that we view to be technically important, with the upper band for the U.S. 30-year yield between 5.0 percent and 5.18 percent, which is a particularly important technical threshold. Specifically, while risk assets such as stocks appear to be discounting a positive resolution to the Iran war, we would view a move by the U.S. 30-year yield above the upper band to be an important signal that investors are viewing inflation as an accelerating risk and a potential catalyst for the equity cycle that began in Q4 2022 to peak. There are two upside bands for the U.S. 10-year yield that we view to be important starting at the 4.5 to 4.6 percent range followed by the 4.8 to 5.0 percent range.

The bottom line technically is that we expect U.S. long-term interest rates to remain in their broad trading ranges through Q2 but encourage investors to monitor the upper technical bands noted above as trigger levels where equity markets are likely to react.