Key points

- The S&P 500 did much better in the rally that followed the U.S. election than major non-U.S. equity markets, but much worse in the recent correction. Investor sentiment has become one-sidedly pessimistic.

- An oversold rebound may arrive in the coming weeks, but moving on to sustainable new highs could require a re-energised earnings picture catalysed by a meaningful scaling back of trade issues.

- Most importantly, the U.S. needs to avoid recession. If it fails to do so, most equity markets are likely to face weaker earnings and share prices than they have experienced so far.

Major stock markets spent much of February and March either correcting (the S&P 500 and other U.S. large-cap indexes) or easing back from recent highs (Canada’s TSX and Japan’s TOPIX) or putting in new highs (the MSCI Europe and UK indexes). The standout over the past few months has been China’s Hang Seng racing to a succession of new cycle highs, admittedly from very depressed lows.

The S&P 500 became oversold by several measures, enjoyed a welcome rebound rally for a couple of weeks, and then retreated again. Whether a more sustainable rally will develop soon that could reach yet another new high remains an open question. It could also be no more than a brief upside interlude, to be followed quickly by some further downside.

Here are a few things to consider. From its all-time high in mid-February, the S&P 500 Index retreated by almost 11 percent at its lowest point. That would make it a garden-variety pullback in the view of Lori Calvasina, RBC Capital Markets, LLC’s head of U.S. equity strategy. What’s perhaps most noteworthy is that over just six weeks some well-watched gauges of investor sentiment swung from too complacently bullish all the way to very—and probably unsustainably—bearish.

One such indicator, the weekly Sentiment Survey by the American Association of Individual Investors, has recently hit depressed lows from which Calvasina points out the S&P 500 has generated average returns in excess of 10% over both nine-month and one-year holding periods.

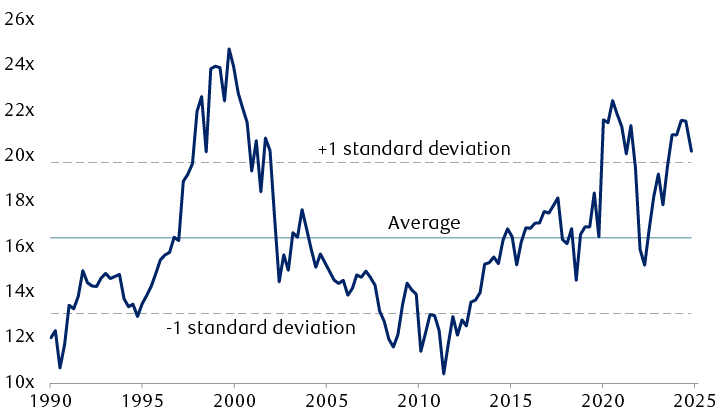

It would be easier to accept and act on these bullish probabilities if valuations (price-to-earnings multiples or P/Es) had fallen to compelling levels, but they haven’t. The forward P/E for the S&P 500, after peaking at 22.8x as the market reached an all-time high in February, has settled back to 20.4x; most would regard this as still rich compared to its long-term average of 16x.

The median P/E within the version of the S&P 500 that excludes the 10 companies with the largest market capitalisations (which largely eliminates the distorting impacts of the high-flying mega-cap growth stocks) has fallen to a more palatable 17.2x, but that valuation level is also above its long-term average of 15x.

S&P 500 price-to-earnings ratio based on forward consensus estimates

The line chart shows the price-to-earnings (P/E) ratio for the S&P 500 Index quarterly from March 1990 through March 2025, as well as the average (16.4x) and 1 standard deviation lines (positive: 19.8x; negative, 13.0x). The ratio fell from 22.5 at the end of 2020 to 15.2 in September 2022, then rose to 21.6 at the end of 2024, then declined to 20.2 in March 2025.

Source - RBC Wealth Management, Bloomberg; quarterly data through 3/31/25

Markets can rally meaningfully from less-than-compelling valuations, but it helps if the underlying fundamental earnings picture is improving—or at least not open to serious question. Of course, today’s ultra-elevated level of policy and economic uncertainty does just that: raise questions about the durability of the earnings outlook.

In the U.S., management confidence is very much in flux, and we suspect the same is true elsewhere. The three months following the U.S. election featured surging CEO optimism about the future, as reported in several well-regarded surveys. But the latest survey undertaken by Chief Executive magazine in early March revealed a sharp reversal in CEO sentiment, giving back all the post-election gains—and then some—to produce the lowest reading since November 2012. Of the CEOs surveyed, 48 percent said they expected a recession or slowdown within six months. Their sidekicks, chief financial officers, have become even more pessimistic: 60 percent of CFOs in a CNBC survey said they expect a recession in the second half of the year. Just one quarter ago only seven percent thought a recession would arrive in 2025.

Both groups say the high level of uncertainty means decisions about pricing, hiring, and capital spending are much harder to make with confidence.

Current valuations of major equity indexes versus long-term averages

| Index | P/E on forward earnings | Long-term average |

|---|---|---|

| S&P 500 | 20.4x | 16.0x |

| S&P/TSX | 15.2x | 14.7x |

| MSCI Europe | 15.5x | 13.6x |

| MSCI UK | 11.2x | 12.3x |

Source - RBC Wealth Management, Bloomberg; data as of 3/28/25

All this fast-rising pessimism could fade away, perhaps as quickly as the post-election enthusiasm mounted. But not overnight. The next important management pulse-taking will get underway in late April as part of the Q1 reporting season. As things stand, we expect that many CEOs will be reluctant to give forward guidance for upcoming quarters, just as they were at the start of the year. Unwillingness to give guidance is rarely interpreted by investors as a positive signal.

So, in the absence of greater clarity, the consensus 2025 earnings estimate for the S&P 500 may be increasingly vulnerable to downward revision. It has already come down by about two percent from the $274 per share where it began the year (which was itself down from a $280 high-water mark set last August). It now sits at $269.

Index earnings estimates typically erode by about five percent over the course of the year. That would put 2025 earnings at something around $260, representing an increase of roughly six percent over 2024’s $245 per share. An erosion in growth expectations of that magnitude would not pose a problem for the market, in our opinion, as long as investors could confidently expect a reacceleration of earnings growth in 2026. And the market’s latest pullback seems to have already priced in the likelihood of that scale of earnings revision. A meaningfully deeper price retrenchment than the S&P 500 has already experienced would probably require a growing percentage of investors and forecasters on the Street to join with CFOs and CEOs in expecting a U.S. recession.

By and large, the forecasters are so far not subscribing to that idea. Most were prompted by evidence of Q1 weakness to lower their full-year U.S. GDP growth estimates to something either side of two percent, but few forecasts of outright recession have surfaced. Consumer and management pessimism about the economic outlook isn’t the same as cutting spending, which has mostly held up for both households and businesses.

In our view, there are plausible paths to new highs for the S&P 500 and other major equity markets. The first requirement would be a catalyst to bring buyers back into the dominant position in the U.S. equity market. We suggested two in this space last month: a peace treaty, ceasefire, or any other agreed downshifting of the Russia-Ukraine conflict; and meaningful scaling back of trade issues.

The latter would be the most important, and would have to be sufficiently impactful to produce changes in several areas: reducing inflationary pressures enough to put rate cuts back on the table for the Federal Reserve; giving businesses confidence to plan, hire, and spend on capex; and boosting consumer confidence by reducing job insecurity.

There is also a necessary condition: the U.S. needs to avoid recession. If it doesn’t, we think an earnings valley is likely to open up that will eventually take share prices lower than they have been so far.

We have repeatedly emphasized the need to have the market’s direction validated by measures of market breadth such as the advance-decline line and the unweighted version of the S&P 500 Index. This is becoming all the more important, in our view, as the recent pullback has raised concerns that a deeper stock market retrenchment may lie ahead if the economy falters.

The jury is still out on this issue. After leading the S&P 500 Index higher all through the powerful market advance from October 2022 to December of last year, those breadth measures have failed to confirm either the January or February all-time highs posted by the S&P 500. They appear close enough to doing so that we believe it’s worth waiting to see if the next rally is accompanied by broad enough participation to get the job done.

Meanwhile, we think this confluence of possibilities calls for investors to remain cautious, watchful, but invested. We are intent on limiting our buying to stocks that have staying power and companies with the least to lose if a recession does materialise.