Key points

- The U.S. dollar is the world’s reserve currency and the backbone of the global payments infrastructure.

- Countries that face restrictions over the use of this system due to sanctions would like to see an alternative.

- If the dollar were to be supplanted, the U.S. would lose many benefits that accrue to the dollar’s reserve currency status.

- The entrenched nature of the dollar in global finance, together with conflicting political goals amongst its detractors, suggests a practical replacement is unlikely.

The mighty greenback has reigned supreme as the world’s reserve currency since at least the abandonment of the gold standard in the 1970s, and likely since the end of World War II. It is also the world’s predominant currency for the transaction of goods and services between nations and trading blocs. The currency has cemented its status with the development of a global payments infrastructure during this time—simply put, it’s hard for countries and multinational companies to wean themselves off the U.S. dollar system.

But the rapid pivot away from liberalized trade agreements toward a multipolar protectionist world brings the dollar’s status back into focus. Sanctions imposed on Russia subsequent to its 2022 invasion of Ukraine raised the hackles of authoritarian regimes across the world as they realized there were few alternatives to the dollar world.

This has led to the idea of de-dollarization—or the goal of creating a competitor to the dollar’s role as both a reserve currency and as a highway system for global transactions.

We look at the challenges of de-emphasizing the dollar and its related global infrastructure and argue that the dollar’s “exorbitant privilege” as a reserve currency and payment system has few realistic challengers.

The more things change, the more they stay the same

The recent drumbeat of angst over the dollar’s status is nothing new. Historically, calls for the dollar to be supplanted as a reserve currency grow louder when one or more of several developments occur. A change in the long-term trend of the dollar’s valuation against other currencies, specifically when a strengthening trend pivots to a weakening trend, often triggers this debate. And U.S. partisan politics can play a part too, particularly if political dysfunction and fiscal woes prompt a downgrade of the country’s credit rating. Increasing geopolitical tensions and generational changes in the global order tend to sharpen the debate, and lastly, rapid technological change can open the door to rivals to the dollar’s status. In our view, all four factors are at play at this time.

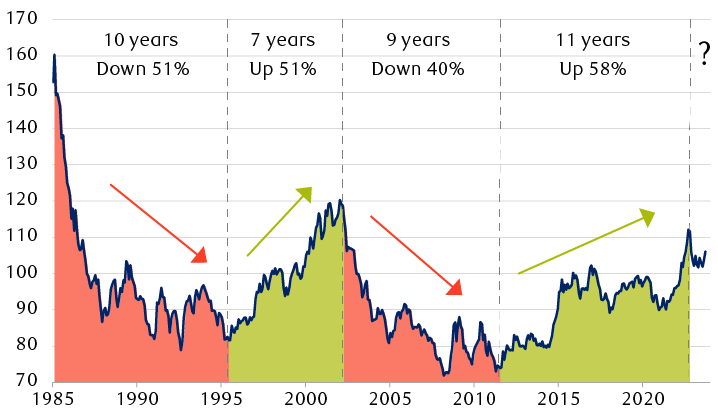

The start of a new dollar bear market? Too early to say

Trade-weighted U.S. Dollar Index (DXY)

Line chart showing the value of the trade weighted dollar index, with four distinct cycles averaging 9 years in length with moves of the order of 40% to 60%. The latest bull cycle may have ended in 2022 after an 11-year run.

Source - RBC Wealth Management, FactSet; monthly data from January 1985 through September 2023

What is de-dollarization anyway?

De-dollarization is the process of reducing the world’s reliance on the dollar as the world’s primary reserve currency and transaction currency for international business. This may occur naturally as technology and global growth provide more alternatives to the dollar, but some countries might want to nudge the process along for their geopolitical advantage.

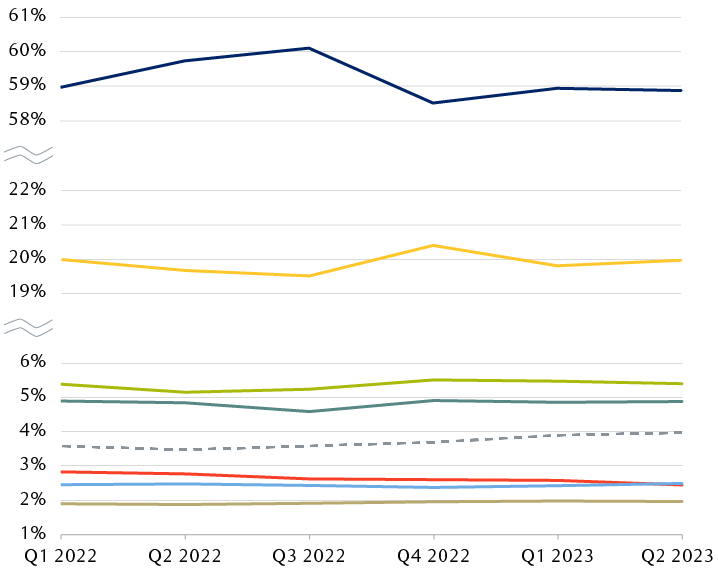

According to the International Monetary Fund (IMF), the dollar accounted for 59 percent of global currency reserves at the end of Q1 2023, down from more than 70 percent in 2001, but still well ahead of the euro at around 20 percent and the Japanese yen at around five percent. And the share of reserves really hasn’t changed much since the start of the war in Ukraine and the U.S. Treasury Department’s associated financial sanctions on Russia.

Contenders vs. pretenders: No big changes in global reserve currencies

Shares of global reserves held in major currencies

Line chart showing the percentage of global currency reserves held in major currencies quarterly from Q1 2022 through Q2 2023. There has been little change from quarter to quarter over this period. The most visible change is a decrease in the U.S. dollar share from Q3 2022 to Q4 2022 (to roughly 58.6% from 60.1%), with a corresponding increase in the Euro (to 20.4% from 19.5%) and to a lesser extend the British pound. The most recent percentages are: U.S. dollar, 58.9%; euro, 20.0%; Japanese yen, 5.4%; British pound sterling, 4.9%; Chinese yuan, 2.5%; Australian dollar, 2.0%; Canadian dollar, 2.5%; other currencies, 4.0%.

Source - RBC Wealth Management, World Bank; data as of 9/29/23

What could replace the dollar as a reserve currency? The two closest challengers, the euro and the yen, have grown their share of reserve holdings, but not to the extent of the dollar’s losses. And while China would like its renminbi to topple the dollar, that currency’s share of global reserves remains a paltry 2.5 percent, although certain authoritarian regimes seem increasingly attracted to the currency. For example, Russia currently holds about a third of all reserves in the Chinese currency.

We don’t think any single currency is positioned to replace the dollar in the global reserve system. Instead, we expect a gradual diversification into the many developed nation currencies of Asia and the rest of the world. Emerging market (EM) currencies will probably need to wait until the financial community develops enough trust in the soundness of EM economies.

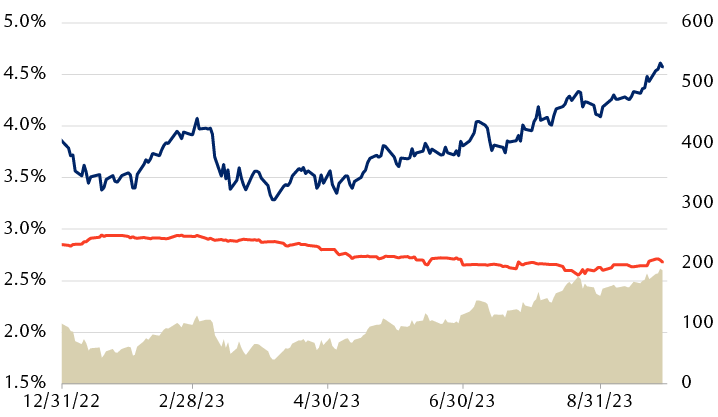

Of course, official reserve accounting may hide the true picture of what’s going on behind the scenes. The U.S. and Chinese bond markets diverged after Q1 2023, with U.S. Treasury yields moving higher as investors sold these bonds and Chinese government bond yields heading in the opposite direction as buyers increased their purchases.

Are diverging yields a sign of de-dollarization? Not so fast

Yields on benchmark 10-year government bonds in the U.S. and China

Line chart showing the daily yields of 10-year government bonds in the US and China, with an added bar chart denoting the difference in yields. While U.S. yields moved higher after Q1 2023, Chinese yields moved lower, with the spread between them growing from 41 basis points near the start of April to 189 basis points near the end of September.

Source - RBC Wealth Management, FactSet; daily closing yields, 12/31/22–9/28/23

This coincided with increasing concerns in the financial media, including Bloomberg, that some sovereign funds were exchanging their dollar reserves for the Chinese currency. We think there’s an easier explanation. This divergence was a result of significant differences between the two economies. A solid labor market and resilient consumer in the U.S. have kept inflation higher than is comfortable for bondholders. Whereas real estate woes and tepid economic growth in China have prompted that country’s authorities to keep interest rates low.

Excuse me, your “exorbitant privilege” is showing

We don’t believe the dollar is at risk of losing its reserve currency status in the foreseeable future. And that’s a view that will be applauded by U.S. policymakers, as this status comes with a lot of benefits. This package of benefits is widely known as “The Exorbitant Privilege,” a term coined by French Finance Minister Valéry Giscard d’Estaing in the 1960s.

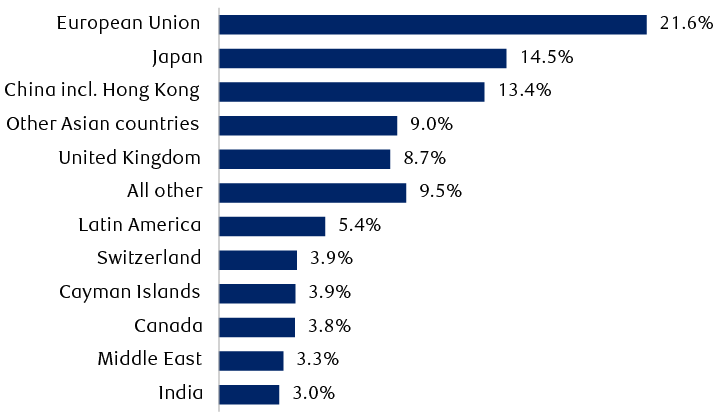

One of the benefits is robust international demand for U.S. Treasury bonds. This demand allows the U.S. government to issue more debt, and at lower rates, than would be the case if the dollar lost its status. Why is demand for U.S. bonds so strong? Because foreign nations need a deep, liquid asset market in which to park their reserves.

The world’s largest savings account?

Share of overseas U.S. Treasury debt holdings by country/region

Bar chart showing the percentage of overseas-held U.S. federal debt by country and region. The largest foreign holder is the European Union with 21.6% of the overseas holdings followed by Japan at 14.5% and China at 13.4%. The rest of the foreign holders are: Other Asian countries, 9%; United Kingdom, 8.7%; All other, 9.5%; Latin America, 5.4%; Switzerland, 3.9%; Cayman Islands, 3.9%; Canada, 3.8%; Middle East, 3.3%, and India at 3.0%.

Source - RBC Wealth Management, U.S. Treasury Department; data as of August 2023

Another benefit is felt via the value of the currency itself. Foreign demand for the dollar depresses the value of overseas currencies, and therefore makes imports cheaper in dollar terms for U.S. consumers. Meanwhile, the foreign exporters get paid for their wares in U.S. dollars that then get invested in Treasury bonds, and so the cycle continues.

So, it would be natural for central bankers in other countries to be envious of this privilege. But these benefits also come with responsibilities. The reserve currency status requires a fully convertible currency and a free-floating exchange rate determined by financial markets. These requirements are unpalatable to some overseas central bankers who prefer to keep their own currency under close control—another reason for the dearth of alternatives to the dollar as a reserve currency.

This flexibility of the dollar cements its status as a reserve currency. It allows it to mop up excesses elsewhere in the world. Currently, there is a glut of savings outside of the U.S., and very little of those excess savings are placed in any currency other than the dollar.

Don’t “buck” the system

It's not just the dollar’s reserve currency status that proponents of de-dollarization are eyeing. Some nations are wary of the world’s reliance on the dollar within the global payments infrastructure. The ease with which the U.S. and its developed nation partners were able to implement asset freezes and sanctions on Russia for its invasion of Ukraine caught the attention of some countries worried they might someday get locked out of the system.

Over the last year, several countries have diversified the payment systems they use to trade goods, with a view to creating an alternative to the dollar’s hegemony in global trade.

Some of the higher-profile examples include Russia and Iran accepting Chinese renminbi for their oil sales. India has also stepped up its use of the Chinese currency, and authorities in Beijing claim that half of their cross-border payments are now conducted in renminbi. This is a natural consequence of the Chinese economy moving up the value chain, but it’s important to note that even with this progress, the renminbi still only accounts for two percent of global cross-border trade transactions and four percent of foreign exchange transactions.

This is because the dollar payment ecosystem offers advantages built up over generations that other currencies can’t provide. These include the ease of raising capital in dollars, and deep derivatives markets that facilitate hedging for global traders. So while there may be demand for alternatives to the dollar payment system, the supply of practical alternatives is likely to remain thin, in our view.

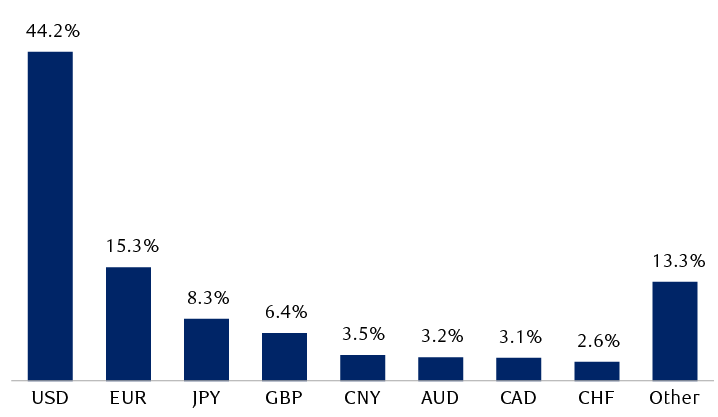

The U.S. dollar dominates the world of foreign exchange

Volume of global foreign exchange transactions by currency

Bar chart showing the share of foreign exchange volume by transaction currency. The USD is the most traded currency, as it is involved in 44.2% of global transactions. The euro is the next most used with a 15.3% share. Additional currencies shown on the chart are JPY, 8.3%; GBP, 6.4%; CNY, 3.5%; AUD, 3.2%; CAD, 3.1%; CHF, 2.6%, and Other, 13.3%.

Source - RBC Wealth Management, Bank for International Settlements; data as of 12/31/22

All in all, it’s just a few more BRICS in the wall

The expansion of the BRICS grouping of developing nations (Brazil, Russia, India, China, and South Africa) announced during the bloc’s annual summit in August 2023 caught the attention of the de-dollarization community, particularly given the tentative discussions toward the creation of a currency basket or some other alternative to the dollar.

However, our view is that the natural geopolitical tensions within the BRICS+ grouping, together with the reluctance of individual members to surrender the sovereignty of their own currencies, makes the advent of a new currency bloc unlikely. We believe the benefits to BRICS+ members derive from their ability to straddle the fence in terms of international relationships in the deglobalizing world and expand trade and investment flows between countries. Any new BRICS financial infrastructure would likely be limited in scope and more of a bolt-on to the existing global financial architecture, at least over the foreseeable future.

Please see this brief commentary for more of our thoughts on the BRICS expansion .

Reports of the dollar’s demise are greatly exaggerated

We believe the increase in calls for a lessening of the greenback’s status as a reserve currency and medium of trade is a natural consequence of the secular trend of deglobalization as weakening demographics and increasing nationalism create rifts in global geopolitics.

However, the dollar’s deeply embedded infrastructure within financial markets and global trade makes it difficult, in our view, for alternative currencies to take a significant share of the dollar’s role on the global stage. We expect the push to de-dollarize to remain in the headlines, but to not significantly alter the status quo over the next several years.