- Enthusiasm for AI and the future economic growth it may be promising, together with central bank cutting, pushed the majority of stocks to new highs this year. There may be more of that to come in 2025, but we believe optimism about the future will need to be buttressed by a continuation of positive economic growth.

- Already-stretched valuations and increasingly frothy investor sentiment readings argue for a cautious, considered approach to equity selection.

The last washed-out low for global equity markets was in fall 2022. Investor sentiment had swung from enthusiastic optimism in January of that year to concerned pessimism at the October lows. From that point, markets turned abruptly higher and never looked back.

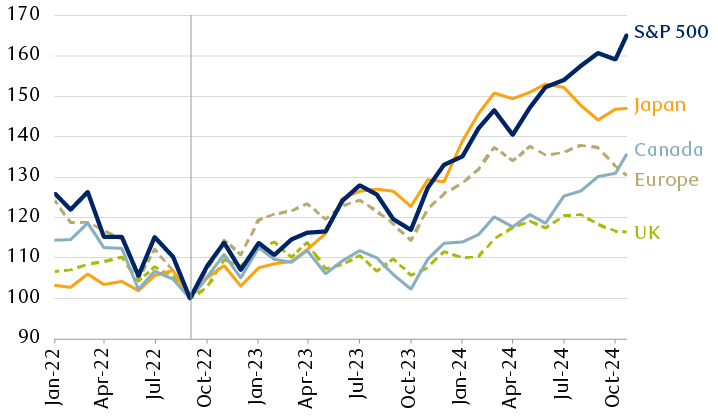

All the major equity markets over the intervening 25 months (China’s aside until recently) advanced sharply, led by the S&P 500 up a remarkable 68 percent.

This steep path higher for the S&P was, to a great degree, forged by the performance of a handful of mega-cap technology stocks whose substantial spending commitments to the development of artificial intelligence (AI) raised the prospect of those companies delivering outsized sales and earnings growth in the years ahead.

Enthusiasm for AI fostered optimism about future economic growth bolstered by central bank cutting, pushing the majority of stocks to a succession of new highs. That can be seen more clearly in the performance of the “unweighted” version of the S&P 500, which removes much of the distortion introduced by the strong-performing, mega-cap Magnificent 7. This equally-weighted index was up a less remarkable but still surprising 48 percent.

The gains posted by the non-U.S. indexes were well above average but more subdued. None contained any of the Magnificent 7 stocks and generally had much less exposure to the Tech sector.

Major indexes have seen two years of “up”

Equity index performance relative to September 2022

The line chart shows the performance of major equity indexes since January 2022, rebased relative to September 2022 = 100. Japan is represented by the TOPIX Index, Canada by the S&P/TSX Index, Europe by the MSCI Europe ex UK Index, and the UK by the MSCI UK Index. All indexes have risen over the period, with the U.S. S&P 500 rising the most, followed by Japan, Canada, Europe, and the United Kingdom.

Source - FactSet; Japan is represented by the TOPIX Index, Canada by the S&P/TSX Index, Europe by the MSCI Europe ex UK Index, and the UK by the MSCI UK Index

Valuations have changed materially as markets have moved higher over two years: the S&P 500 rose by 68 percent but the index earnings per share was up by a comparatively meager 12 percent. That leaves the price-to-earnings (P/E) multiple at 24.7x (trailing 12 months), up by half from the 16.4x at the October 2022 low.

There is no convincing line in the sand beyond which equity valuations cannot venture. With consensus earnings forecast to rise by 14.6 percent to $276 in 2025, we think it would not be unreasonable to look for new index highs again next year nor out of the question for the P/E multiple to move beyond the almost 25x (trailing) touched this year.

Recession realities

Equity markets tend to keep moving in the prevailing direction until something forces a turn. Corrections come and go unpredictably and usually don’t last too long, with the market recovering any lost ground quickly. Bear markets, on the other hand, take longer to play out and entail deeper (albeit temporary) price declines. For more than a century, these deeper downturns have always been associated with a U.S. recession.

The window can’t yet be closed on the possibility of a recession arriving as a consequence of the Fed tightening cycle. Recessions have started an average of 10 quarters after the first Fed rate hike. We are now in the 11th. In more than half the recessions, the first-hike-to-recession gap was longer than the 10-quarter average.

Of course, it’s also possible no recession arrives, which would leave the bull market with further to run. There are two market-related measures in particular we are monitoring to gauge whether or not the market is running out of steam.

One is market breadth—are the majority of stocks moving in sync with the broad averages? The answer to this continues to be yes. New highs in the S&P 500, the Dow Jones Industrial Average, and the NYSE Composite, including those set in early November, have all been matched by new highs in their respective advance-decline lines and associated “unweighted” versions of the S&P 500 and Dow. Historically, market breadth has usually turned lower before the capitalization-weighted indexes have reached their final peaks in a bull market. No such negative divergence has appeared. As long as breadth measures and major market indexes remain in sync, we would expect to see more new highs for equity markets.

We are also paying attention to investor sentiment, which has been no more than moderately optimistic over the past year. Recently, however, some sentiment indicators have been giving frothier readings. For example, a measure of bullish positioning in the stock futures market, compiled by RBC Capital Markets’ U.S. Equity Strategy team, has recently set new all-time highs while in The Conference Board’s October Consumer Confidence Survey, 51.4 percent of respondents “expected stock prices to increase over the year ahead,” the highest reading since the question was first asked in 1987.

Some of this elevated investor enthusiasm could be U.S. election-related and might recede in the coming months. If it doesn’t, the combination of persistent excessive optimism and the one-sided positioning noted above might suggest that those who want to be in are in. New buyers will be needed, and that often requires a period of lower prices and more compelling valuations.

Much depends on the consensus 2024 S&P 500 earnings forecast of $241 per share and 2025 forecast of $276 per share holding together. As RBC Capital Markets, LLC’s Head of U.S. Equity Strategy Lori Calvasina notes, “there is room for market valuations (P/Es) to expand somewhat further but not a ton.” It is our view that investors have already paid once, and generously, for these earnings prospects and may well balk at paying again.

In our view, even if more serious downside and a recession that would put that downside into play can be avoided, the road to higher equity prices from here will require some threading of the needle while leaving investors to contend with occasional pullbacks along the way.

Watchful, cautious, invested

We expect breadth and sentiment will help us determine which path prevails in the coming months. In our view, the appropriate positioning for the year ahead in a global balanced portfolio would have equities at, but not above, the long-term target exposure. Our mantra has been and continues to be “watchful, cautious, but invested.”

Beyond the outlook for 2025, powerful trends will likely continue to play out in the global economy and could have important portfolio implications.