The eye-watering movement in global central bank rate expectations and sovereign bond yield pricing this week comes on the heels of what has already been a significant repricing within bond markets since the war in the Middle East began in late February.

Sharply higher energy prices are, of course, the core driver of global markets at the moment. As a result, the primary focus of central bankers this week was on the interplay of the impact of higher energy prices on inflation and the potential for a negative impact on economic activity and labor markets.

Markets appear to believe that when push comes to shove, the potential upside risks to inflation will outweigh the downside risks to growth, particularly for regions that are net oil importers and for central banks with a singular mandate of price stability, as opposed to the U.S. Federal Reserve with its dual mandate of price stability and maximum employment.

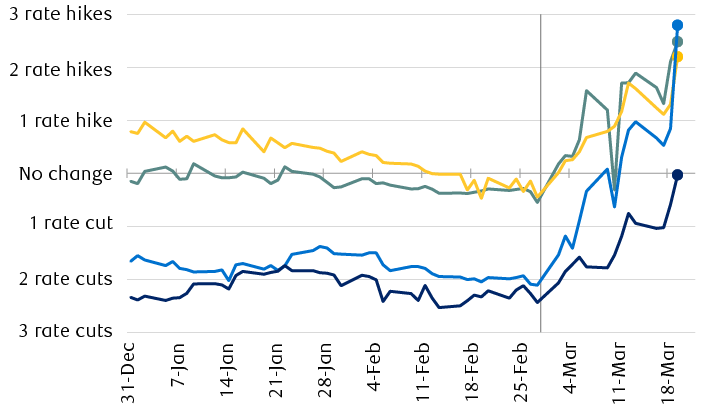

Market pricing flips from rate cuts to potential hikes

Market-based estimates of 2026 interest rate decisions

Vertical axis crosses at start of Iran conflict (2/28/26).

Source - RBC Wealth Management, Bloomberg

The chart shows the evolution of market-based expectations for central bank interest rate decisions since the start of 2026. Markets are now expecting just over two rate hikes from the Bank of England, European Central Bank, and the Bank of Canada. Markets expect the U.S. Federal Reserve to remain on hold this year with roughly zero rate cuts now priced.

The Bank of England (BoE) was the most explicitly hawkish this week, stating that policymakers “stand ready to act” on inflation, which has had a material impact on global bond markets this week. Markets are now pricing slightly more than two 25 basis point rate hikes by the end of the year—with similar expectations now implied for the Bank of Canada (BoC) and the European Central Bank (ECB). Whereas the Fed’s Federal Open Market Committee (FOMC), which sets policy rates, was previously projected to cut twice this year, markets now see it keeping rates unchanged.

While not as significant on a global scale, it was notable that the Reserve Bank of Australia (RBA) raised rates for a second consecutive meeting, while the Bank of Japan (BoJ) held rates steady—though we expect it to proceed with its ongoing modest rate hike campaign next month.

What might central banks be facing?

RBC Capital Markets, LLC Global Head of Commodity Strategy Helima Croft recently laid out a couple of scenarios for oil prices. Should the conflict persist for three to four weeks, Brent oil prices could exceed the $128/barrel peak level from 2022 in the aftermath of Russia’s invasion of Ukraine. Should the war expand and extend for several more months, then oil prices could eclipse the 2008 record high of $146/barrel.

With respect to inflation, RBC Economics projects that if oil prices average $100/barrel this year it would add about 0.75 percent to headline inflation, with annual rates peaking this year at 3.00 percent and 3.50 percent for Canada and the U.S., respectively.

For central banks, the typical playbook is to look through energy price shocks, particularly short ones, as the feed-through to core inflation (excluding food and energy) is generally minimal. However, if sustained, higher energy prices will eventually impact costs throughout corporate supply chains, to say nothing of the potential risks of higher business and consumer inflation expectations—risks that may be amplified in this episode given the inflationary environment that has persisted for nearly five years now.

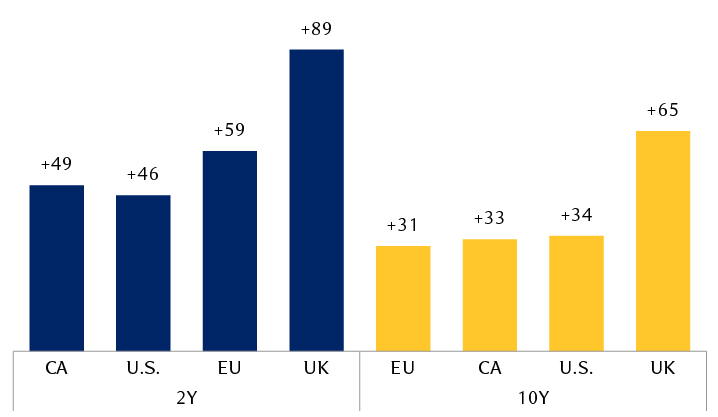

Change in sovereign bond yields since Feb. 27, 2026

Basis points

Source - RBC Wealth Management, Bloomberg; Europe represented by German Bunds

The chart shows the change in benchmark 2-year and 10-year sovereign bond yields for Canada, the United States, Europe (represented by German Bunds) and the United Kingdom since just prior to the start of the Iran war. For 2-year bonds, Canada is up 49 bps, the U.S. is up 46 bps, Europe is up 59 bps, and the UK is up 89 bps. For 10-year bonds, Europe is up 31 bps, Canada is up 33 bps, the U.S. is up 34 bps, and the UK is up 65 bps.

Oil prices in the driver’s seat, as Powell makes plans to stay in his

Of the major global central banks, the Fed is perhaps the most insulated from the current global backdrop, but it’s not immune.

The FOMC’s first update of the year to its economic and interest rate projections was somewhat confusing, in our view. Policymakers, on average, upgraded both the inflation and growth outlooks while leaving the unemployment outlook unchanged—but still projected one rate cut this year regardless.

However, we can probably cut the Fed some slack on the forecasting front, as Chair Jerome Powell noted in his press conference, if ever there was a quarter to skip the forecasts given all the uncertainty (something it did only once in 2020), this would probably have been the meeting to do so.

In terms of market-moving developments, it was perhaps Powell’s declaration that he plans to stay on as Fed chair until the Department of Justice’s investigation into his testimony regarding the Fed’s headquarters renovation is “well and truly over,” and would be willing to continue on should his replacement not be confirmed by the end of his term in May. He further stated that though he has not yet made a decision as to whether he will opt to serve out his term as Fed governor through 2028, he will make his decision based on the best interests of the institution.

The subsequent rise in Treasury yields perhaps implies that markets believe Powell is both more likely to stay on for at least somewhat longer, and to act as a significant counterbalance against political pressure to lower interest rates absent the requisite economic justification.

Our base case in our 2026 outlook was already that the Fed would keep rates on hold this year. We see no reason to change that view but see the bar for rate hikes as exceptionally high.