The renewed crisis in the Middle East—the largest in scale since the U.S. military interventions in Iraq and much wider in scope has already impacted global energy markets and precious metals prices and threatens equity markets.

While the situation is extremely fluid just days into the conflict, we are assessing developments very closely along with our RBC Capital Markets partners.

Following are key excerpts from multiple reports that two important RBC Capital Markets experts have written in recent days about the crisis, with an emphasis on global energy markets and the U.S. equity market.

Helima Croft | Head of Global Commodity Strategy, RBC Capital Markets LLC

Potential impact on energy prices: Conflict duration is key

The ultimate energy price trajectory will hinge on the duration and degree of disruption emanating from this conflict. Certainly, if the war is over in a few days, the oil risk premium will likely recede.

- In a prolonged conflict scenario, we see oil prices reaching into the $100s per barrel, as we and regional experts warned, and global [natural] gas prices could at least hit their highest since the first quarter of 2023.

- It is our understanding that regional leaders warned Washington about the contagion risks of another confrontation with Iran and indicated that $100+/barrel of oil was a clear and present danger. With Washington having declared a maximalist regime change goal, the Islamic Revolutionary Guard Corps (IRGC) may believe it can prevail in a war of attrition if President Donald Trump is not prepared to commit ground forces. Some military planners have warned that air power alone has rarely yielded a complete regime change outcome, even if decapitation of the top layer of leadership is achievable without boots on the ground.

- We also think officials in Washington could come to regret not refilling the Strategic Petroleum Reserve (SPR) if this proves to be a longer duration conflict. China, by contrast, has been aggressively filling its strategic reserves, potentially due to supply disruption concerns. Again, if this proves to be a short exchange of fire, any oil price increase will likely prove fleeting, and market participants will refocus on the fundamentals. On the other hand, prices will likely move materially higher if this conflict extends beyond a few days and if the IRGC pursues a survival strategy predicated on exploiting President Trump’s economic pain points.

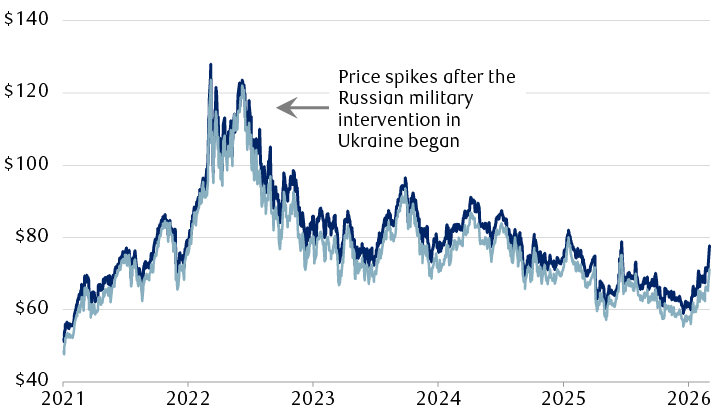

Amid the Middle East crisis, oil prices have bounced off of low levels recently

Crude oil futures prices per barrel in U.S. dollars

The line chart shows Brent and West Texas Intermediate crude oil prices from January 2021 through March 2, 2026. Both oil types traded in a similar pattern during the period. They began at $51.80 and $48.52, respectively. They rallied and started 2022 slightly under $80. They spiked to above $120 per barrel in March 2022 following the Russian intervention in Ukraine, then pulled back a bit, and traded back up above $120 in June 2022. Prices then drifted lower into mid-2023 to roughly $70. They subsequently traded in a wide range, but with a lower trajectory, reaching $67 and $62, respectively by mid-February 2026. Both have bounced off the low levels, ending the period at $77.74 and $71.23, respectively, on March 2, 2026.

Disrupted: Strait of Hormuz oil and LNG transit

- While Iran has not yet officially stated its aim to close the Strait of Hormuz, tanker traffic through the all-important waterway has already been significantly curtailed following the recent targeting of vessels in the strait and in the Gulf of Oman. Flows on Sunday [March 1] reportedly were reduced to a mere seven tankers and one gas carrier, with three shadow fleet tankers included in that figure, whereas Friday [February 27, before the initial strikes] saw 56 tankers navigate the strait. Though the IRGC may not be able to physically close the Strait of Hormuz, we maintain that they are able to adequately deploy small boats, mines, drones, and missiles to ensure insurers and shipping companies continue to avoid the waterway until the cessation of hostilities. Most major insurers will reportedly officially terminate war risk coverage for the waterway on March 5 at midnight London time.

- There have been conflicting reports from the White House about overall strategy. Some administration statements suggest a desire to restart negotiations, while others point to a willingness to undertake a multi-week military campaign. The latter would increase the likelihood of a much higher [energy] price scenario if there is no viable plan to ensure the freedom of navigation through the Strait of Hormuz. Above all, we would caution against recency bias. Working off the June 2025 script [when the previous military clash between the Israel/U.S. and Iran occurred], some market participants may have misjudged Iran’s willingness to use asymmetric tactics to internationalize the costs of the joint Israeli/U.S. military action and ensure regime preservation.

- It has already been reported that Iraq’s Foreign Minister Fuad Hussein spoke with his Saudi counterpart about the risks of the strait remaining closed. Faced with material storage limitations, Iraq would likely have to start shutting in production if it cannot utilize the waterway for its 3.5 mb/d of southern exports.

The European natural gas index has been highly sensitive to previous supply constraints

Dutch TTF Natural Gas Futures per megawatt-hour (MWh) in euros

Source - RBC Wealth Management, Bloomberg; data through 3/2/26

What about other energy transit routes in the region?

- Though there are some oil pipeline outlets that could theoretically moderate the full impact of the closure of the Strait of Hormuz, such as Saudi’s East-West pipeline (7 mb/d capacity) and UAE’s Abu Dhabi Crude Oil Pipeline (ADCOP) pipeline (1.5 mb/d capacity), by a few million barrels a day taking into account current operating rates, significant risks and limiting factors exist. We would emphasize that both assets remain at serious risk of being caught in the crosshairs of the conflict themselves, in which case damage could eliminate this option entirely. There is precedent for such attacks, as we saw in the 2019 targeting of the East-West pipeline by Houthi drones, which damaged two pumping stations and temporarily downed crude flows through the route. Furthermore, rerouted exports via the Red Sea would similarly be vulnerable. We would also note that some regional producers lack any potential alternative routes, such as Kuwait and southern Iraq.

Why OPEC production increases could be a moot point

- Moreover, the absence of serviceable sea lanes essentially renders any production increase an entirely moot point, as the lion’s share of OPEC barrels in the region could essentially become stranded assets in an extended war scenario.

- In our view, every OPEC+ producer is essentially maxed out with the sole exception of Saudi Arabia. Hence, the barrel impact of any headline OPEC+ increase will be limited by the lack of actual production capabilities. Moreover, any surge above levels produced in the April 2020 price war peak would likely necessitate tapping storage. Even then, the utilization of any spare barrels will be severely limited if critical waterways are rendered inoperable. Spare barrels serve little purpose if there are no serviceable sea lanes.

Iranian military strike capabilities

- While there has been considerable focus on Iran’s missile stockpile, we believe that the country’s extensive unmanned aerial vehicle (UAV) capabilities may provide it bandwidth to continue asymmetric attacks and move the conflict up the escalation ladder. Some leading military experts are already drawing comparisons to the Russia-Ukraine conflict, with both sides deploying UAVs to conduct disruptive infrastructure attacks and to make up for missile stockpile shortfalls. Tehran has already launched its cheap and domestically produced Shahed family of one-way drones against a variety of targets across the Middle East this weekend [February 28–March 1], including U.S. bases and civilian sites in Bahrain, Iraq, Kuwait, Qatar, and the UAE.

Lori Calvasina | Head of U.S. Equity Strategy, RBC Capital Markets LLC

For the U.S. stock market, it all may come down to the oil market

- When it comes to stocks, it still may mostly come down to the oil market. We’ll leave the oil price forecasting to our colleagues in Commodity Strategy & MENA Research who are monitoring the situation with the Strait of Hormuz [see above] … we’ve been constructive on U.S. equities in 2026 and that remains our view today. But we do think it’s important to keep a close eye on oil market dynamics given that there has been an inverse correlation of -40% between the S&P 500 and oil prices since COVID [beginning in the first quarter of 2020]. In our view, the key issue is not whether there is a short-term spike in oil prices. What’s more relevant to stocks, in our opinion, is whether a sustained impact to oil prices is seen, which is what we think would have more of a potential to damage confidence at various levels.

Equities started to reflect the risks ahead of the actual beginning of the conflict

- The U.S. equity market was already starting to digest the escalation in the region coming into the weekend [February 28–March 1]. The S&P 500 has moved sideways so far in early 2026, reined in by a fairly long list of concerns—AI fears, private markets concerns, an underwhelming reporting season, extended valuations, and an increase in a few different flavors of geopolitical risk … we think it’s fair to say that both the choppiness in the S&P 500 this year and the outperformance of the Energy sector were reflecting heightened geopolitical risk to some degree.

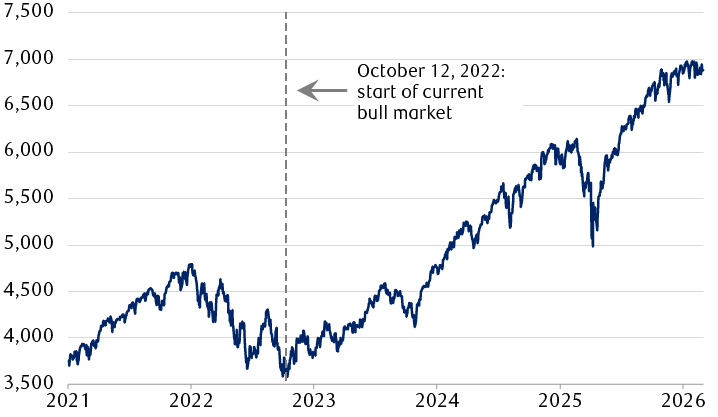

The U.S. stock market has been consolidating recently at lofty levels following a big bull market rally

S&P 500 Index

Source - RBC Wealth Management, Bloomberg; data through 3/2/26

Valuations could come under pressure

- Elevated geopolitical uncertainty isn’t good for S&P 500 price-to-earnings (P/E) multiples broadly, which have already been under pressure. Whenever geopolitical uncertainty spikes, the first thing that usually jumps into our mind is that forward P/E multiples tend to come under pressure for the S&P 500. This speaks to one of the transmission mechanisms of geopolitical conflicts and risks to equities … in recent years we’ve seen some deterioration in S&P 500 median P/Es when uncertainty regarding national security has spiked in the spring of 2025 (Liberation Day tariffs), the first quarter of 2022 (Russia’s invasion of Ukraine), and the first quarter of 2020 (COVID). This is something we also saw in early 2003 as the U.S. was preparing to invade Iraq.

Keeping an eye on corporate and consumer sentiment

- Elevated geopolitical uncertainty/risk has become a feature of the post-COVID environment, but could weigh on sentiment. We are primarily thinking about the read-through of geopolitics to corporate sentiment (where uncertainty has improved but remains elevated), given that references to geopolitics on public company earnings calls have been extremely high in recent years relative to their pre-COVID history … but for now expect the “manage through” messaging to persist [meaning, corporate leaders have previously, repeatedly indicated they are managing through external challenges]. Putting corporates aside for the moment, we will also be monitoring how these latest developments in U.S. foreign policy impact consumer confidence/sentiment (which has been stabilizing around extremely low levels in both the Conference Board and University of Michigan surveys) as well as public opinion polls (where voter approval on foreign policy has been low).

Be careful with historical stock market performance studies

- We’d be careful paying too much attention to historical studies that suggest always buying stocks on bad geopolitical news. Note that we are constructive on the U.S. equity market this year, but [our study of prior episodes] reminds us that it is very difficult to look at geopolitical events in isolation when it comes to the stock market. What’s happening with geopolitics is usually a piece of a larger puzzle.