Key points

- In late 2024, we identified four long-term investable themes: the gray wave, AI spending, renewables, and electrification, all set to experience predictable, long-term demand growth.

- To these we now add medical advances and defense spending.

- These six unstoppable themes should provide portfolios with investable opportunities capable of delivering long-term compounding of sales, earnings, and share prices for decades.

Eighteen months ago, we offered some thoughts on four investable themes we expected to have legs for at least the next two decades:

- The surging “gray wave” of retirees with mostly fixed incomes, who are facing rising costs of care and have an appetite for therapies and products promising to lengthen healthspans (i.e., the number of years a person lives in good health);

- Massive AI spending by both tech and non-tech businesses driven by the unacceptably high cost of being left behind; and

- The emergence of electricity as the dominant source of power enabled by the rapidly declining costs and scalability of renewables (wind and solar) as well as grid-scale power storage.

To these we are adding medical advances as another Unstoppables theme. There have been at least two transformative tools developed in the last 15 years—the so-called CRISPR biological gene-editing tool and Google DeepMind’s AlphaFold protein-mapping application—that both rapidly accelerate and expand researchers’ ability to identify, design, and deliver promising therapies, some of which have now started to arrive.

We are also adding defense spending triggered by the geopolitical eruptions of the past few years and months, together with the U.S. insistence that its allies carry more of the shared financial burden as well as the indications that it is rethinking its commitments to the defense of Europe and perhaps Taiwan, or indeed much of East Asia. The same forces are driving many nations to reconsider food and energy security.

All of the above are driven by demand imperatives that show very few if any signs of abating. For at least the next two or three decades we believe they are likely to provide a reliable, exploitable tailwind for some businesses, and perhaps challenging headwinds for others.

The gray wave

A growing elderly population around the world will have to be cared for. It has also become a large addressable market for a range of goods and services.

Economists, sociologists, and governments have been watching the inevitable approach of a massive gray wave for a couple of decades—now it’s here. In all the major economies (and most of the rest) the proportion of the population over the age of 65 is already surging to levels never seen before. Even the over-80s cohort, once an insignificant minority, is rapidly becoming a component to be reckoned with.

The global population of people 65 years and older will approach 1.6 billion by 2050, according to the UN. The cost of caring for a fast-growing segment that is no longer earning employment income is a problem desperately in need of solutions.

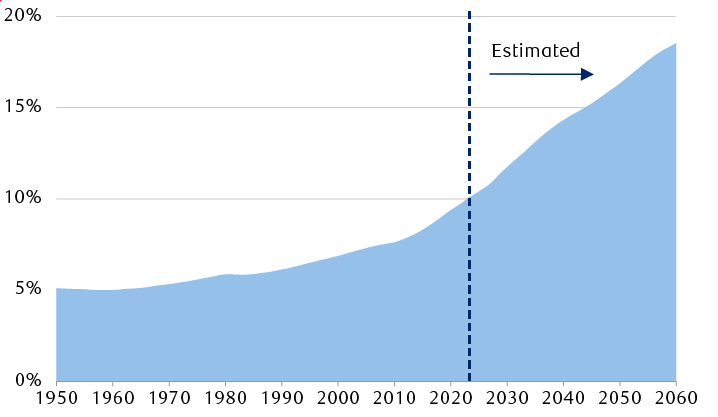

Percentage of world population over age 65

Source - RBC Wealth Management, United Nations

The chart shows the historical percentage of people aged 65 and over in the world population. In 1950, people over 65 represented roughly five percent of the total population. By 2024, that proportion was roughly 10%. The UN estimates that by 2060, nearly 20% of the world population will be aged 65 and over.

The Alzheimer’s Association estimates that in 2025, total health care costs for all individuals in the U.S. 65 years and older suffering from Alzheimer’s disease reached $409 billion, or considerably more than cancer and cardiology care combined. It also points out that millions of family members and unpaid caregivers provided 19.3 billion hours of care, valued at $446 billion in 2025. Given these onerous costs borne by both governments and households and that up to 20 percent of life is spent battling chronic diseases in later years, scientists are focused on lengthening healthspans (i.e., the number of years a person lives in good health).

Investable ideas

- The financial services industry (e.g., wealth management and insurance) as individuals will need to consider how not to outlive their savings;

- Homebuilders looking to meet increased demand to accommodate both multigenerational households and single-occupancy homes;

- Travel (e.g., air and rail operators, cruise lines, and recreational vehicle manufacturers) and recreation/leisure (e.g., gardening and DIY tools and supplies) as these areas are top of the to-do list for most planning to retire.

Medical advances

Roy Amara, an American scientist and futurist, observed what came to be called Amara’s Law: we tend to overestimate a technology’s impact when it first arrives on the scene, but underestimate what it actually delivers a decade or so later. The Gartner Hype Cycle maps the same phenomenon: inflated expectations peak and disillusionment follows, before a plateau of productivity eventually emerges. The medical sector illustrates the different facets of Amara’s Law.

Short-term overestimation

- In the early 2020s, Google DeepMind’s AlphaFold cracked a key biological puzzle: predicting the shape of over 200 million proteins, including some 20,000 proteins encoded by human genes. Proteins need to fold into the correct three-dimensional shape to function; knowing that shape is essential to understand disease and design appropriate treatments. The work earned AlphaFold scientists the Nobel Prize in Chemistry in 2024 and prompted ambitious predictions well before that AI could eliminate disease within a few years, which sadly remains a distant prospect.

- The CRISPR gene-editing technology was heralded as a potential cure for genetic diseases when it emerged in the early 2000s, also winning its developers a Nobel Prize, before disappointing as costs ran into millions of dollars per patient and progress stalled.

- Personalized cancer vaccines face a similar challenge. Custom-designed for each patient’s unique tumor profile, they remain prohibitively expensive. However, by using AI to dramatically accelerate the identification of individual tumors, personalized cancer vaccines are becoming increasingly viable, with potential approval from the U.S. Food and Drug Administration within the next two years, subject to positive results from final-stage clinical trials.

Long-term underestimation

- The shingles vaccine was deployed for decades to prevent a painful skin condition. Unexpectedly, in 2025, scientific journal Nature reported that the vaccine can also reduce the risk of developing dementia by 20 percent over a follow-up period of seven years. The long-term impact of a technology can exceed initial expectations—and in completely unexpected ways.

- After more than a decade, the first approved CRISPR-based therapy for humans arrived in 2023 (for sickle cell disease), though it remains beyond the financial reach for most patients for now. The disease, painful and debilitating, has an estimated eight million sufferers and 100 million carrying the trait, according to The Lancet, a medical journal.

- CRISPR-based technologies are also providing new therapeutic avenues for beta thalassemia, a condition that requires a lifetime of frequent blood transfusions.

- There is also early promise from a small trial that has showed a dramatic slowing in the progression of Huntington’s disease, regarded as incurable.

- Also of note, following the injection of CRISPR-modified pancreatic cells into an individual suffering from Type 1 diabetes, the patient’s pancreas produced normal insulin for more than a year without rejection.

Early disappointment has not always been the end of the story. Medical advancements tend to retain their momentum, and with AI accelerating progress across several fields simultaneously, we believe the long-term potential of today’s technologies is likely to surprise on the upside.

Investable ideas

- Biotech companies that prioritize diseases with a meaningful unmet need and demonstrate the ability to execute on well-designed clinical trials.

AI spending rolls on

AI may prove to be a textbook illustration of Amara’s Law. Near-term expectations seem to have outpaced reality, though the underlying improvements in AI models suggest to us that the long-term impact could still be underestimated.

Escalating AI infrastructure spending

Spending on the development and application of AI will accelerate further from today’s already lofty levels as tech companies—from “mega” to “mini”—struggle to avoid being left irretrievably behind.

- Based on their most recent announcements, AI-related capital spending by the Magnificent 7 (Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA, and Tesla) is expected to grow by a whopping 75 percent in 2026 to $668 billion, representing a substantial two percent of U.S. GDP. Further increases are planned in 2027 and 2028.

- RBC Global Asset Management Inc. Chief Economist Eric Lascelles points out that these figures have been revised significantly higher since the beginning of the year. Compared to projections as of December 31, 2025, combined Magnificent 7 capital spending estimates for 2026, 2027, and 2028 have risen by $166 billion, $231 billion, and $275 billion, respectively. That is, the total expected capital spending over the next three years (2026 inclusive) has risen to $2.31 trillion, a 41% increase over what had been planned just four months ago.

- Many investors reasonably question whether a bubble may be forming, but Lascelles suggests that such skepticism may not be warranted. Since 2020, the compute required to train models has grown by roughly five times annually. Meanwhile, training costs are rising at three-and-a-half times per year, and power requirements are doubling annually. Yet, according to METR, an AI research institute, the complexity of tasks AI models can handle independently has grown approximately sixfold since 2024, suggesting that the return on AI infrastructure investment may be improving, as model capability continues to outpace cost increases.

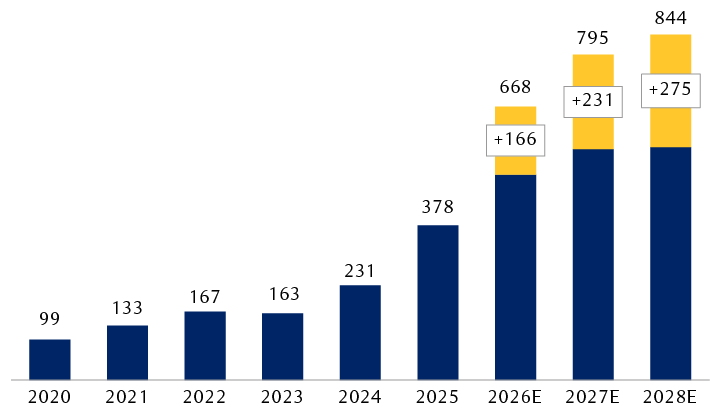

The Magnificent 7 have significantly increased their capex plans this year

Magnificent 7* capital expenditure estimates ($ billions)

*Alphabet, Amazon.com, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla.

Source - RBC Global Asset Management, Bloomberg; data as of 5/1/26

The chart shows actual and estimated combined annual capital expenditures by “Magnificent 7” technology companies (Alphabet, Amazon.com, Apple, Meta Platforms, Microsoft, NVIDIA, and Tesla) from 2020 through 2028. For 2026, 2027, and 2028, the chart shows estimates as of December 31, 2025 as well as the amount of new estimated spending added as of May 1, 2026. The totals are: 2020, $99 billion; 2021, $133 billion; 2022, $167 billion; 2023, $163 billion; 2024, $231 billion; 2025, $378 billion; 2026, $668 billion (increase of $166 billion); 2027, $795 billion (increase of $231 billion); 2028, $844 billion (increase of $275 billion).

In Lascelles’ view, on this basis, tech executives’ optimism does not seem misplaced. It likely reflects genuine confidence in AI returns, rather than speculative bubble dynamics. Nevertheless, whether rapidly improving models can generate revenues that justify current spending levels remains an open question.

AI infrastructure expenditure played a significant role in offsetting growth headwinds from tariffs in 2025. It contributed approximately 0.5 percent to U.S. GDP growth, largely offsetting the roughly 0.75 percent drag from tariffs. Lascelles expects a similar contribution in 2026.

Uptake by non-tech businesses just getting started

The U.S. Census Bureau’s Business Trends and Outlook Survey data (to May 2026) shows that overall AI usage for the companies surveyed hovered between 17 percent and 20 percent—and that between 20 percent and 23 percent of businesses that have yet to use AI expect to use it in the next six months. These numbers are up significantly from the end of 2024, but not appreciably from the end of last year.

As of May 3, 2026, AI usage rates in the Information (39.7 percent) and Finance and Insurance (33.9 percent) sectors were both higher than the national rate (19.8 percent), according to the Census Bureau, but significant shifts have not been reported in these sectors since December.

In comparison, businesses in the Retail Trade sector reported current and expected usage rates below the national average: around 14 percent of businesses currently use AI, and about a further 17 percent expect to in the next six months. The Manufacturing sector was also below average in adoption, with current and expected use at 17 percent and 19 percent, respectively.

The Census Bureau estimates that only 0.1 percent to 0.2 percent of U.S. firms use AI to automate a large number of human tasks. Over 90 percent of companies using AI report zero employment changes.

Executives outside the Technology sector speak enthusiastically about what they expect AI will do for their businesses. But comparatively few, so far, can point to any sustainable return on investment from these expenditures. In our opinion, that won’t stop or slow down the spending anytime soon—most businesses perceive the cost of being left behind as unacceptably high. But, at some point, returns will need to justify the AI expense.

For now, most companies committed to this spending argue that the high experiential gains may prove vital to remaining competitive in the future. Underspending remains the riskier strategy, in our view.

Investable ideas

- AI equipment manufacturers and the computer chip complex have been the clear beneficiaries of the new technology, with their stock valuations having expanded markedly. We think investment portfolios would likely benefit from exposure to the infrastructure beneficiaries of generative AI (GenAI)—e.g., electricity production, transmission, and storage, as well as data center construction and data transmission—where the eventual spending may take a decade or more to arrive.

- Shares of companies that adopt the new AI solutions may also benefit, but we believe investors should assess how the technology is being implemented—to increase sales, reduce costs, or improve productivity—and keep an eye on the competition. If competitors are also using GenAI effectively, any competitive advantage may erode quickly.

For more on this theme, please see these articles from our “Innovations” series: Generative AI: enablers and adopters and Exploring the impacts of AI and GenAI across industries .

The relentless march of renewables

Kick-started by government subsidies more than two decades ago, the rapid installation of wind farms, solar collectors, and now energy storage facilities have driven down the cost of renewable power (without subsidies) to levels that have already made renewables the lowest-cost energy sources in many countries.

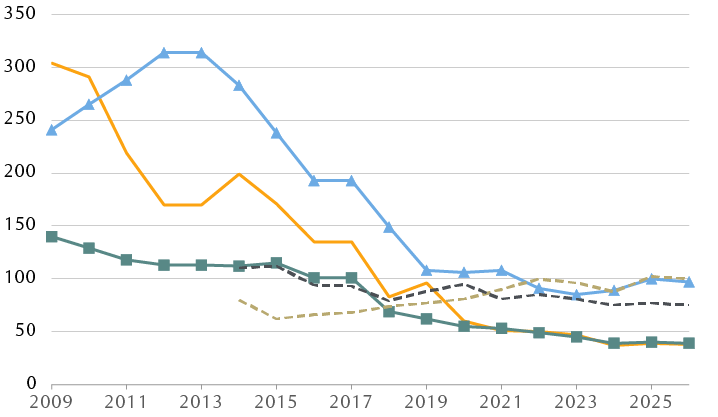

Solar and onshore wind are cheapest electricity sources

Global levelized cost of electricity (LCOE), $ per megawatt-hour

LCOE is the long-term breakeven price a power project needs to recoup all costs and meet the required rate of return. LCOEs do not include subsidies or tax credits. Figures have been adjusted for inflation and expressed in 2025 U.S. dollars. Photovoltaic fixed are static solar panels mounted at a fixed angle.

Source - RBC Wealth Management, BloombergNEF

The chart shows the all-in cost of operating generation assets that use different energy sources (coal, natural gas, wind turbines located onshore and offshore, and solar) over the period 2009 to 2025 and estimates for 2026. For all energy sources, the cost has declined markedly, with offshore wind and solar experiencing the steepest decline. Solar and onshore wind are now the least expansive ways to generate electricity.

Renewable energy sources provided nearly 26 percent of U.S. electrical generation in 2025, as well as over 36 percent of installed generating capacity. The International Energy Agency (IEA) projects solar, wind, and battery energy storage to add over 60 percent more generating capacity in 2026 than in 2025.

Close to one-third of China’s electricity consumption now derives from renewables and an even higher 49 percent in Europe, as of 2025. The adoption of renewables will almost certainly continue, in our view, thanks to striking cost advantages.

For more than a decade, global installation of new solar power generation has routinely exceeded the IEA’s five-year forecasts, sometimes by 100 percent or more. The Global Solar Council estimates that global installed solar capacity has reached almost three terawatts—that is, three trillion watts or the equivalent of some 10 billion solar panels installed—enough to power 1.5 billion homes. That is triple the installed capacity reached only four years ago. The permit approval backlog is substantial and growing, suggesting to us that growth of new renewable power installations is not likely to slow appreciably anytime soon.

Investable ideas

- Renewable energy equipment manufacturers

- Providers of energy storage, energy efficiency, and/or smart grid solutions

The electrification of everything

Falling costs for renewable energy, combined with rapidly expanding installed capacity, are laying the groundwork for a significant rise in electricity consumption—particularly as the intermittent nature of wind and solar is addressed. BloombergNEF estimates that solar will become the largest source of electricity globally by 2032 with wind not far behind.

Technical, managerial, and systems engineering improvements have been changing the design and management of traditional power grids to accommodate renewable sources. But the rapid expansion of utility-scale storage facilities, in the form of so-called grid-scale batteries, is making the raw cost advantage of solar and wind that much more compelling by addressing the issue of intermittency.

Today, giant batteries arranged in rows of containers have become a preferred technique to store power, as their cost has fallen dramatically. BloombergNEF estimates there will be more than two terawatts of stationary battery storage installed globally by 2035. Meanwhile, advancements in battery technology and chemistry are driving innovation. Promising alternatives include sodium-ion and nickel-hydrogen batteries, as well as vanadium flow batteries.

Energy is a major input cost for many industries, businesses, and households. Getting plentiful, low-cost renewable energy from where it is produced to where it is needed is a major industrial enterprise on its own. Grid-scale batteries can enhance energy resilience, balancing fluctuations in supply and demand.

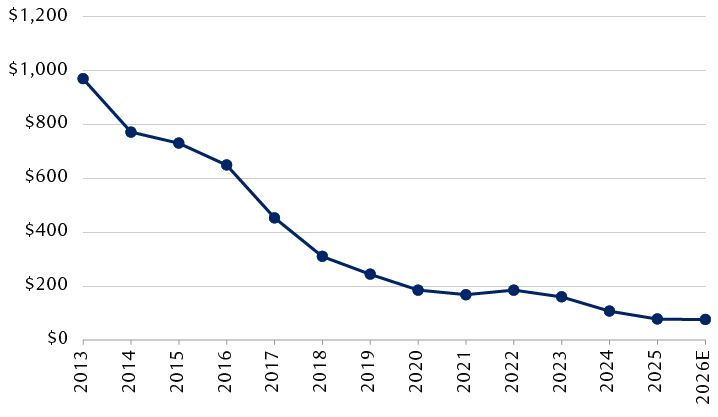

The cost of utility-scale batteries has fallen more than 90% in 12 years

Four-hour utility-scale battery storage costs, $ per megawatt-hour

Source - RBC Wealth Management, BloombergNEF; costs in 2025 dollars

The chart shows the cost per megawatt-hour of a four-hour utility-scale battery system in 2025 U.S. dollars from 2013 to 2026 (estimated). From nearly $1,000 in 2013, the cost decreased to roughly $200 in 2020; since then, it has decreased more slowly, reaching an estimated cost of approximately $75 in 2026.

Investable ideas

- Raw materials such as copper, nickel, lithium, cobalt, and uranium;

- Electrical generation and transmission equipment, including transformers, switches, high voltage cables, solar panels, and electrolyzers;

- Software solutions to enhance grid balancing (i.e., so that electricity consumption matches electricity production of an electrical grid); and

- Specialized engineering and construction businesses.

Defense spending

Higher defense spending should persist for years largely due to the ongoing transitioning from a U.S.-led Western unipolar order to what is often described as a multipolar or polycentric world order. Sole U.S. dominance, which had characterized much of the post-Cold War period, is morphing into a new framework where not only the U.S. and Western-aligned countries shape global affairs, but China, Russia, India, and Iran, among others, also have significant influence.

The tension between the unipolar and multipolar frameworks could play out for many years or even a couple of decades. The transition is already proving to be turbulent and disorderly. The Russia-Ukraine war, with the U.S. and NATO backing the latter; the U.S. special forces raid in Venezuela; the U.S./Israel war in Iran; and the Trump administration’s attempt to assert more control over global energy flows and shipping lanes are among the initial links in this chain.

Amid this transition, major, middling, and some smaller military powers seem committed to robust weapons spending and, in many cases, expanding their armed forces. The U.S. is calling upon Europe, Canada, Japan, and South Korea to shoulder more of the defense burden. Even Germany and Japan are pushing against foundational post-World War II agreements that limit re-militarization.

For starters, the U.S. and European NATO countries seek to rebuild stockpiles of existing weapons systems due to significant depletions during the wars in Ukraine and Iran. A study published by the Washington D.C.-based Center for Strategic and International Studies think tank in May 2026 assesses that it could take years to replenish U.S. stockpiles; Pentagon leadership has acknowledged this. It follows that U.S. resupplies to Europe, Japan, and South Korea could take even longer, in our view.

Additionally, and importantly, major military powers and some others are prioritizing the development of advanced precision weapons systems, which we think will be in high demand in the future.

Investable ideas

- Aerial and sea drones and other autonomous vehicles: Technological leaps are evolving over just weeks or months amid real-time battlefield feedback.

- Artillery complexes: While some have argued artillery is becoming a thing of the past due to drones, we believe this couldn’t be further from the truth.

- Standoff precision air-launched cruise missiles and high-capacity guided bombs: These are staples in any modern conflict.

- Offensive ground- and sea-based ballistic, cruise, and strategic missiles, especially those that fly at hypersonic speeds and have maneuvering capabilities: The U.S. and European countries have a lot of ground to make up in these areas.

- Missile and drone defense: Western-aligned countries also lag in the all-important missile defense category.

- Intelligence, surveillance, and reconnaissance (ISR) systems: The U.S. leads in ISR due to its robust satellite system.

- AI, neural networks, advanced algorithms and signals processing, along with netcentric platforms: These technologies are already being integrated into weapons and battlefield management systems.

Long-lasting and powerful effects

There’s plenty we don’t know about how the world’s economy is going to play out over the next 30 years. But there are several aspects where we can identify demand imperatives likely to be in play for at least the next few decades driven by: unavoidable demographics, the delayed arrival of the fruits of advances in biology and life sciences, the arrival of powerful new computing applications, the very rapid and ongoing shift in energy economics, and the inevitable global geopolitical frictions arising from the fracturing of the unipolar world into a multipolar one that is very much in flux.

Identifying reliable long-term sources of demand growth should point the way toward investable sectors and industries that provide the prospect of long-term compounding of sales, earnings, and share prices.