How property passes

First, you need to understand how property passes at death. With this understanding you can properly arrange your assets to pass as effectively and efficiently as possible.

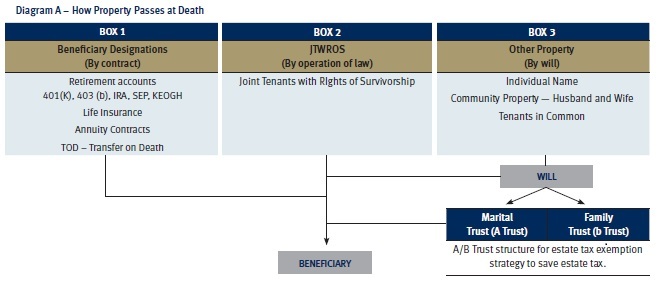

In diagram A below, the type of assets in box 1 pass to heirs based upon their beneficiary designation. The assets included in this category include retirement accounts such as 401(k), 403(b), IRA, SEP, KEOGH, etc. In addition, accounts that have a TOD (transfer of death) provision attached to the account have in essence named a beneficiary. Other assets that have named beneficiaries include life insurance contracts and annuity contracts. Therefore, it is very important to carefully consider how your beneficiary designation is listed. This designation will dictate how the assets are to be transferred to your heirs. Only if you have named “my estate” as the beneficiary do the terms of your will dictate how these accounts are to be transferred.

If you have assets that are titled joint tenants with rights of survivorship (JTWROS) then you have in effect also given this asset a beneficiary designation. As box 2 of the diagram illustrates, the assets will transfer to the surviving joint tenant(s) listed on the title of the account/asset.

Assets in box 3 include assests titled in your individual name, as community property between a husband and wife, or tenants in common. In order to determine how and to whom these assets are to be distributed, we have to look at the decedent’s will. Often, this may be the first time that your executor has picked up your will to look at your instructions. Box 1 and 2 trump your will and, therefore, the assets will flow to the designated beneficiary or the surviving joint tenant not according to your will. However, box 3 is likely the most important box in your estate plan. It is through your will that the tax savings family trusts are created. (Family trusts are also known as exemption equivalent trusts, credit shelter trusts and bypass trusts.)

Family trust

It is often desirable for the decedent to have their property held in an irrevocable trust for the benefit of their surviving spouse and/or children. The family trust would hold the decedents assets up to the exemption amount in the year of death. This technique allows the decedent to have these assets passed to heirs free of estate tax. In states that have enacted a state estate tax, the exemption trust often has two pieces: the federal exemption amount and the state exemption amount. Additional benefits of the family trust include creditor/ predator protection of the assets for the beneficiaries as well as control by the decedent of the ultimate disposition of the assets to heirs.

Marital trust

Any property of the decedent in excess of the exemption amount is often left to the surviving spouse outright or via a marital trust. While this trust does not avoid the estate tax at the death of the surviving spouse, it does have the benefits of creditor/predator protection and control of the ultimate disposition of assets to heirs by the decedent. The exemption equivalent and marital trust outline in your will is commonly referred to as an marital/family trust technique.

Cornerstone documents

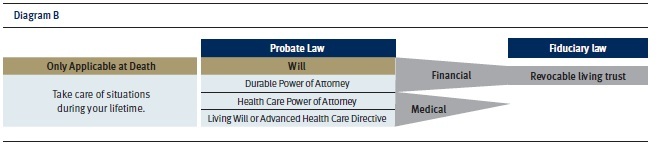

Now that we understand how property transfers at death, let’s review the four cornerstone documents that everyone should have in their estate plan. Please review diagram B.

Will

A will outlines your wishes of how and to whom property is to pass at your death. This may include the establishing of the marital/family trust strategy outlined above — it may include trusts for the benefit of children and/or grandchildren. It may also include specific bequests to individuals and charities. Basically you can include in your will your desire of how your assets are to pass.

Durable power of attorney

A durable power of attorney allows you to appoint an agent to act on your behalf if you are unable to act for yourself with regard to financial matters. It is recommended that you name an agent and at least two successor agents to serve in the event the first agent you have named is also unable or unwilling to serve.

Health care power of attorney

Health care power of attorney allows you to appoint an agent to act on your behalf for medical decisions if you are unable to make those decisions for yourself due to incapacity. This document is vital in the planning documents. It is recommended that the medical power of attorney include a HIPAA release. This release will allow the doctors, hospitals, and other care providers to release your medical information to your agent so they can make an informed decision on your behalf. Without a signed HIPAA release, the doctors, hospitals, and other care providers will be unable to release this data by law.

Living will

A Living Will (or Advanced Health Care Directive)outlines your wishes to be followed by your family and medical care providers in the event you have a terminal illness or are in a vegetative state. This important document allows you to outline your desires for food, hydration, pain medication and/or the concept of dying with dignity.

Revocable living trust

Some individuals choose to have their estate plan outlined in a Revocable Living Trust. In essence, a Revocable Living Trust combines the two financial documents of your plan: your will and your durable power of attorney. Rather than having your finances controlled by an agent your finances are controlled by a trustee. Both techniques will carry out your estate plan.

Using a will and durable power of attorney means that your estate will be overseen by a probate court. The main reason for this stems from the fact that “agents” don’t have a specific set of laws to follow. Therefore, if a beneficiary is somehow harmed by the actions of an agent, their remedy is via the court systems / probate court. In contrast, a revocable living trust has a trustee appointed which is bound by fiduciary duty or sometimes referred to as the prudent person rule. Since these rules exist there is no requirement for a probate. It is, however important to note that durable power of attorney ends at death.

Conclusion

The key to estate planning for your family at this point is flexibility. We know that laws will continue to change and you need to be able to modify your plan based upon a new environment or changes in your personal situation. RBC is here to help with our professional estate planning and trust services. Contact us now for more information.

Additional resources:

Lifetime Gifting: Non Charitable Stretch Your IRA Wills, Probate and Estate Settlement