Declining inflation trends have been established across much of the global economy, with tighter monetary policy proving effective in managing inflation—so far. Inflation measured by the U.S. Consumer Price Index (CPI) has fallen six percentage points since its June 2022 peak. RBC Economics expects this trend to continue, and forecasts the headline inflation rate falling to 2.3 percent y/y and Core CPI inflation (which excludes food and energy) declining to 2.5 percent y/y by Q4 2024.

However, the hotter-than-expected January U.S. inflation data reported this week underscore risks that inflation could drift higher, or remain sticky and above the Federal Reserve’s two percent y/y target for a prolonged period. The CPI rose 3.1 percent y/y in January, ahead of the 2.9 percent y/y consensus forecast, while the Core CPI increased 3.9 percent y/y and has barely budged since October. Financial markets responded to the data with volatility; equities fell and bond yields rose to a lesser degree, highlighting that inflation risks and their consequences still merit close observation.

We think these inflation risks should be incorporated into a broader investment strategy. Specifically, we see opportunities in pockets of global debt markets.

Do supply chain challenges fuel inflation risks?

Although we view global supply chain disruptions as a fairly benign inflation risk in and of themselves, we think rising geopolitical tensions warrant attention given their potential to produce supply disruptions and a sustained decline in global manufacturing activity.

While the challenges facing global shipping today are different than the logistical backlogs associated with the COVID-19 crisis, the resurgence of geopolitical pressures in the Middle East has forced many vessels to avoid the Red Sea and Suez Canal passage. The result has been a meaningful rise in global commercial shipping costs.

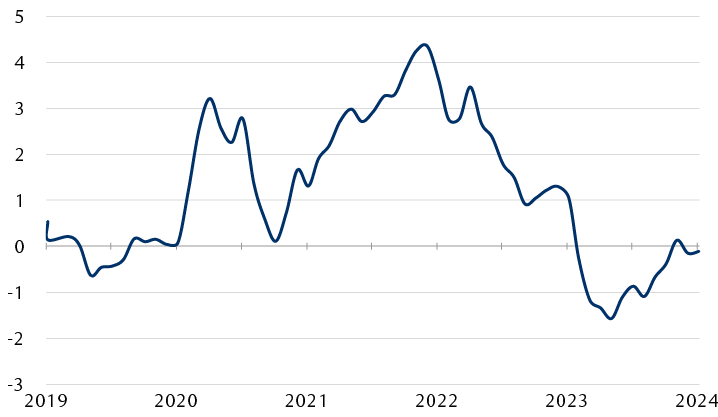

Supply chains: under pressure but still smooth

New York Fed’s Global Supply Chain Pressure Index

Line chart showing the New York Federal Reserve's Global Supply Chain Pressure Index from 2019 to 2024. The index is an aggregate measure that provides insight into whether supply chain pressures, or logistical challenges are improving (a measure below zero), or worsening (a measure above zero). Currently, the chart shows that supply chain pressures have improved meaningfully since the COVID-19 pandemic but have begun to normalize since logistical challenges materialized as a result of the Red Sea attacks on commercial shipping.

Source - RBC Wealth Management, Bloomberg; data through 1/31/24

These regional tensions also raise the potential for elevated energy prices as market participants grow concerned over the insecurity of future supply—or the prospect of outright supply scarcity.

On the production side, elevated input costs and sluggish goods demand have induced a contraction in manufacturing activity throughout the global economy. This contraction has been exacerbated by a broad and protracted slowdown in China’s manufacturing sector, which supplies a sizeable portion of global goods. And due to the integrated nature of Sino-European industrials, similar trends have materialized in Europe’s manufacturing sector.

Labour shortages in certain service-oriented portions of the U.S. economy have also aggravated service sector capacity issues.

If goods and services are short in supply and logistical challenges worsen, consumer prices may rise, particularly if demand conditions evolve.

Robust consumer demand conditions—especially in the U.S.—pose inflationary risks at this point of the business cycle and may push central banks to stay hawkish, in our view. The buildup of excess savings, sturdy wage growth, and a healthy labour market in developed countries have strengthened household balance sheets. This points to a continuation of strong consumption levels, and could give goods and services providers leeway to raise prices without materially suppressing demand.

Higher corporate pricing power can prove inflationary, but a high degree of concentrated demand can also create imbalances. This was shown following the COVID-19 crisis when household spending shifted from goods to services.

Policy risks: Cut and protect?

We see the premature loosening of monetary policy and a longer-term (secular) rise in trade protectionism as key risks to declining inflation trends. Central banks in developed economies have remained committed to achieving their objectives with policymakers generally acknowledging these risks, as evidenced by their recent pushback against markets’ dovish rate cut expectations.

That being said, there is a risk that policymakers may prematurely stimulate the economy with interest rate cuts before inflation is anchored at target levels. Even in a well-intentioned bid to avoid recession, stimulative policy that is executed too swiftly, or incorrectly, could reignite excess demand and fuel inflation.

In addition to monetary policy risks, the shift away from globalization towards more fragmented and politicized trade relations has provided a tailwind to inflation. Geopolitical realignment and populism have increased G7 countries’ propensity for trade protectionism. Wars in Ukraine and the Middle East, as well as heightened Sino-American tensions in a busy election year, have increased policy uncertainty and further accelerated the shift towards more fragmented trade relations. Tariffs on imports—which are essentially tax levies—and general trade protectionism risk dissolving the cost-saving effects of global trade and driving prices higher.

Fixed income shock absorption

Fixed income valuations have undergone a larger adjustment than equity valuations and provide a return profile that is compelling, in our view, irrespective of the inflation outcome. More specifically, we see opportunities in developed-market government bonds given their low risk profile and competitive returns relative to corporate credit.

If inflation rises or remains above target, we think current elevated yield-to-maturity levels provide shock-absorption potential for portfolios in the event that yields rise in response to new inflation premiums.

Elevated bond yields offer solid shock-absorption potential

Bloomberg U.S. Aggregate Investment Grade Bond Index

Line chart showing the yield to duration ratio for the U.S. Aggregate Investment Grade Bond Index from 2003 to January 2024. This ratio represents the upward change in yields (downward move in bond prices) required over the next 12 months for the bond index to generate a forward 12-month return of 0.0%. This allows fixed income investors to appropriately assess the potential downside that could be realized if bond yields rise. In March 2022, we estimated that U.S. investment-grade debt markets only had a 20-30 basis point (bp) shock absorber. Today, because of higher interest rates, inflation, and shifting term premiums, investment-grade debt markets have developed an 85-100 bp buffer, in our assessment.

Source - RBC Wealth Management, Bloomberg; data through 1/31/24

One way to illustrate this capacity to absorb higher inflation is through a ratio known as yield to duration. This ratio represents the upward change in yields (or, conversely, the downward movement in bond prices) required over the next 12 months for a bond index to generate a forward 12-month return of 0.0 percent. This allows investors to appropriately assess the potential downside that could be realized if bond yields rise.

In March 2022, we estimated that U.S. investment-grade debt markets only had 20 to 30 basis points (bps) of shock absorption. Today, as a result of higher interest rates, inflation, and shifting term premiums, investment-grade debt markets have developed a buffer of 85 to 100 bps, in our assessment.

Higher starting yields in fixed income create an opportunity to prepare portfolios for a wide range of potential economic outcomes. Robust shock absorption, elevated yields, and an improving quality of aggregate global debt markets continue to provide some sanctuary from inflationary risks in portfolios, in our view.